A quick update on passenger volumes in Europe

A rather depressing end to the year

Normal seasonal weakness has combined with lock-downs in Europe to deliver rock-bottom passenger volumes in November. We don’t yet have statistics for December, but I thought I’d provide a quick update on the numbers we have so far for the end of 2020.

The low-cost carriers have moved into hibernation mode

Passenger volumes have faded away at the low-cost carriers. After getting up to a peak of 50-60% of 2019 levels in August, November passengers were less than 20% of 2019 levels at Ryanair and Wizz. We don’t have passenger figures yet for easyJet, but they have pulled so much capacity that they must be even lower. The chart below assumes that easyJet achieve load-factors equal to Ryanair for October and November.

Source: Company reports, easyJet figures for October and November are GridPoint estimates based on OAG capacity data and assumed load factors.

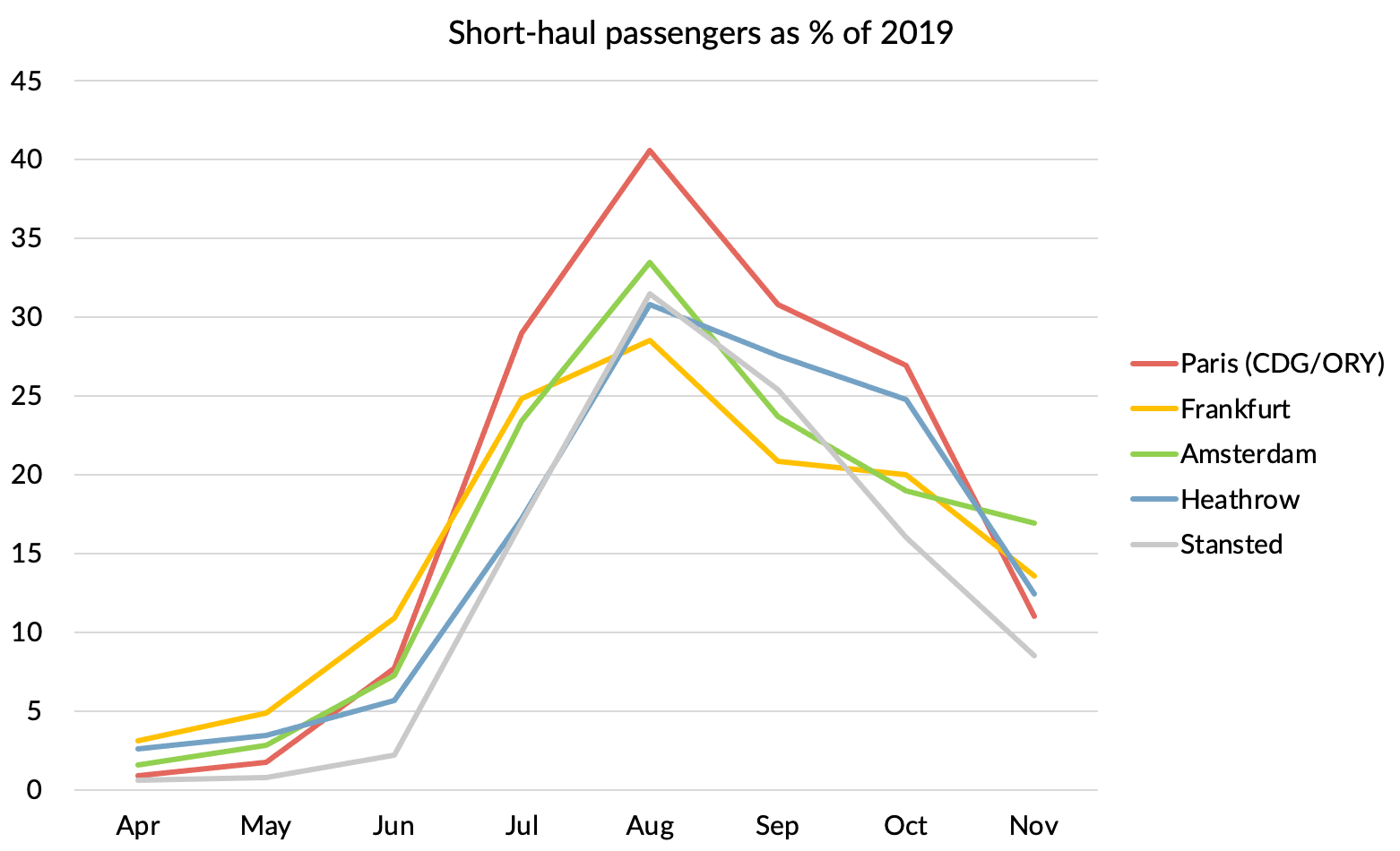

The big hubs are now delivering similar numbers to the low-cost carriers for short-haul

Short-haul passenger numbers as a % of 2019 at the big European hubs were a little lower in the summer than those achieved by the low-cost carriers. That is easily explained by the lack of connecting passengers to long-haul. Since then, they have also fallen back. However, November volumes were quite similar to the low-cost carrier levels. Low-cost carrier dominated Stansted was actually the worst performer in the month.

KLM is pushing connecting passengers hard at Schipol. Connecting passengers reached 62% of all passengers at the airport in November, up from 37% in 2019. That helped move it to the top of league table for short-haul passengers versus last year in the month, taking over from Paris as the strongest performer.

Source: airport statistics

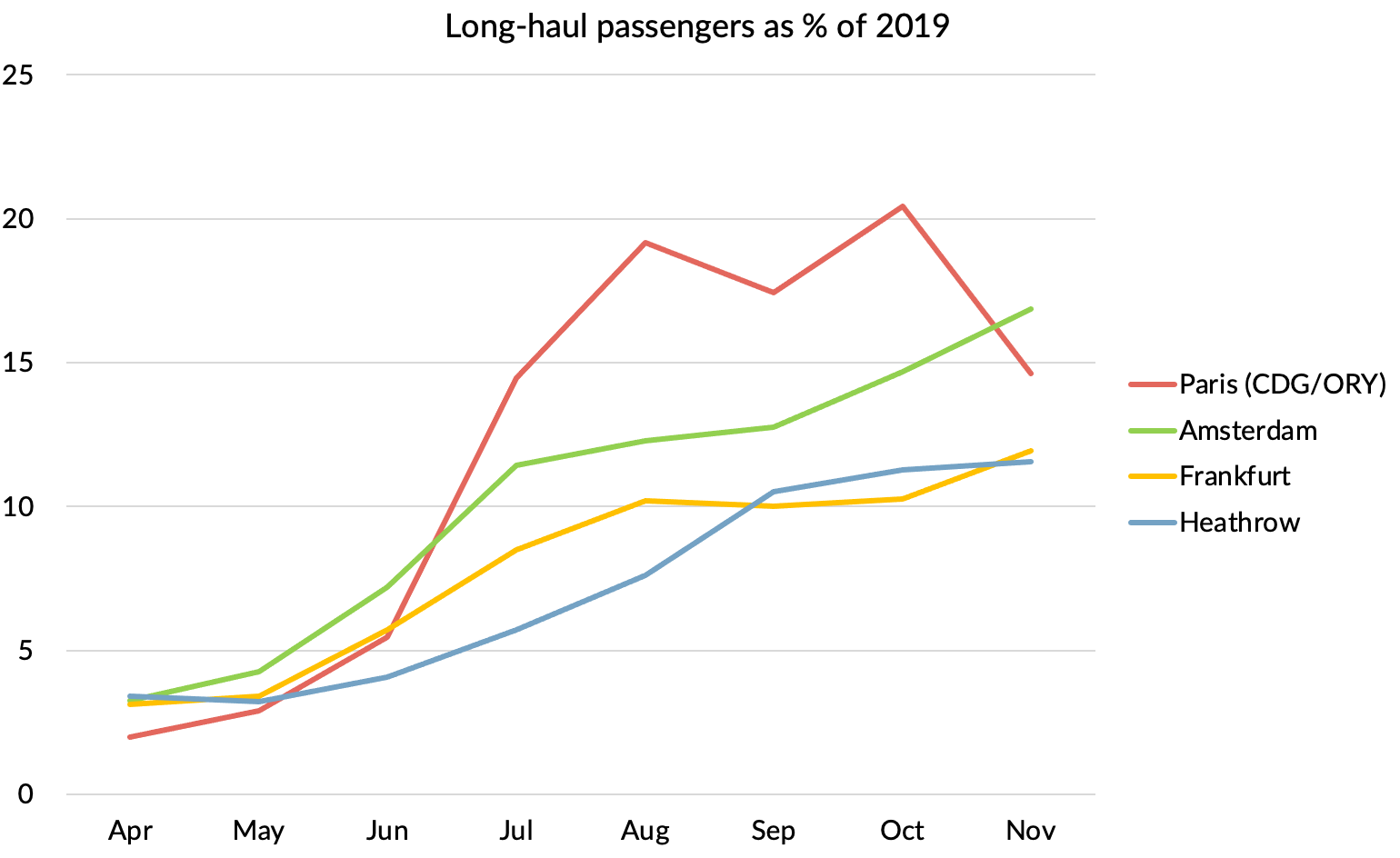

Long-haul passenger volumes are now no worse than short-haul

Interestingly, long-haul passenger volumes have continued their slow recovery and are now no worse than short-haul (10-20% of last year). I’m sure that was driven by winter-sun destinations, with people escaping the rather depressing place that Europe has become during the second wave. Paris was being propped up by the French overseas territories in earlier months. That market has now fallen away and was down 68.6% on last year in November. That has brought to end what had been a period of marked over performance for Paris. Top spot is now occupied by Amsterdam.

Source: airport statistics

What about December?

Source: Eurocontrol

Based on Eurocontrol daily updates on flight being operated (see chart above), most of December was just as bad as November, if not worse. There looks to have been a small uptick in flights in the run up to Christmas, but prospects for December passenger volumes don’t look great either.

A dismal end to a dismal year.