2024 End of Year Review

The state of the aviation nation

It is the time of year for reflection on the year that has just passed, and perhaps a little peering into the crystal ball for what the new year might have in store for us.

Regular readers of my blog will know that I tend to focus heavily on financial metrics of success when judging how well airlines are doing, although in recent times my focus on sustainability has increased as it has risen up the industry’s agenda. Rather conveniently, IATA has just published its annual review with lots of data and analysis on both topics and I’ll be making lots of references to their numbers in what follows. If you haven’t already done so, you might want to pause and read the paper yourself before continuing, in which case here is a link to it: Global Outlook for Air Transport - December 2024.

For those of you who took the time to read IATA’s 36 page document, congratulations and welcome back. For those that didn’t, you really should. It’s an excellent report and covers a lot of ground. Still here? OK, I’ll try and summarise. Written as it is by IATA’s economists, it is full of “on the one hand, but on the other hand…” commentary. Profits in 2024 were relatively good by historical standards with a record net profit of $36.6 billion, but since that only represents a 3.6% net margin, returns are still below the cost of capital. Lower oil prices have reduced industry costs, but that will play through into lower prices over time. Passenger volumes hit new records, but supply has been constrained by aircraft delivery delays, negatively impacting fuel efficiency and causing inflation in leasing rates and maintenance costs. Progress has been made on sustainable fuel volumes, but scaling up production has been slower than was expected last year. Harry Truman’s longed for one-handed economist is still very much missing in action.

Whilst there is no way I can cover everything from the IATA report, I do want to dig into a few of these issues, starting with profitability.

European airline profitabilty

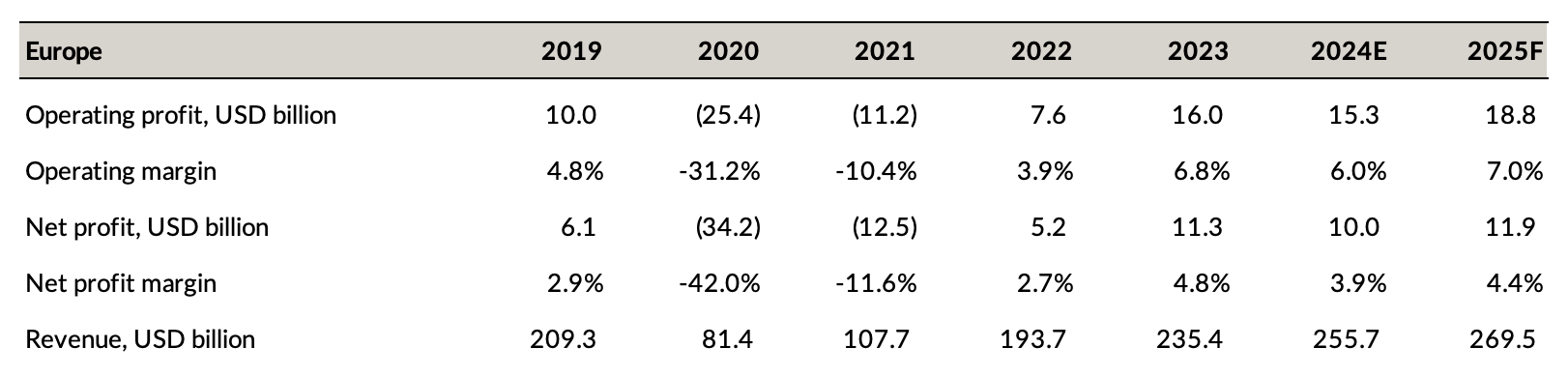

My focus is mainly on Western European aviation, the part of the market I know best. So I’m going to focus on IATA’s profitability figures for Europe, which I’ve reproduced below for convenience. IATA don’t give figures for revenue directly, but you can calculate the figures from the margin information. I’ve taken the midpoint of the estimate you get from the operating margin and the net profit margin figures.

This time last year, I spent quite some time trying to replicate IATA’s historical figures and I’ve gone back and updated that analysis. I added a few more airline companies in an attempt to better match the group that I think are included by IATA (said to be “all commercial airlines”). Jet2, Air Europa, El Al, Icelandair, LOT and TUI Group were added as a result. There are still a few IATA member airlines from Europe that I can’t get figures for, whereas IATA may have the numbers and include them. The public information available is also a bit sketchy for some of the carriers like ITA and Air Europa, for example only providing figures for EBITDA rather than operating profit (a small tip: any carrier that only gives EBITDA figures is losing money but doesn’t want to admit it). So I’ve had to make estimates in a few cases. Nevertheless, I think it is fair to expect a pretty close match.

When it comes to the 2024 forecast, most of the airlines publish quarterly results and in most cases I’ve estimated the full year figures by assuming that the relationship between the full year and the first 9 months follows the same pattern in 2024 as it did in 2023. For the small airlines where we are lucky if we get a single press release a year with any figures (looking at you LOT and Air Europa), I’ve generally assumed that 2024 would replicate 2023. SAS also stopped reporting useful numbers when it was taken private so I’ve also assumed the same results as 2023. I did assume that ITA results would improve, based on the first half EBITDA being reported to be €130m better than the previous year.

I’ve been able to reproduce the IATA revenue figures for 2023 and 2024 pretty well, with my bottom-up exercise totalling $226 billion for 2023 and $247 billion for 2024, in both cases within 4% of IATA’s numbers. The remaining difference could be down to IATA having access to figures for a few additional small carriers.

I had less success with replicating the profit figures. For operating profit, I got $18.8 billion for 2023 (c.f. IATA’s $16 billion) and $16.9 billion for 2024 (vs $15.3 billion). The net profit figures I got were also consistently around $2.5 billion higher than IATA’s, at $14.2 billion for 2023 and $12.4 billion for 2024. With the revenue figures being fairly close, this results in my overall profit margin figures being 0.8 to 1.5 percentage points higher than IATA’s.

What explains the “missing $2.5 billion”? I really don’t know. I’m only missing about $8.5 billion of revenue, so those other carriers would have to be wildly loss-making to account for the difference. The figures for 2023 are all actual results, with the exception of a couple of small airlines where I had to estimate operating profit from EBITDA numbers, so that can’t be a big source of mismatch. For most airlines, it wasn’t a year where there were lots of big one-off exceptional items impacting results, the treatment of which could give rise to material differences.

The only tricky judgements were how to treat $1.4 billion of non-cash currency losses at Aeroflot and $2.6 billion of non-cash deferred tax gains at Turkish Airlines, mostly related to a big inflation adjustment (recent inflation has been super high in Turkey). In both cases I left them out. They work in opposite directions however, and in neither case affect the operating profit figures. There were also $1.6 billion of accounting gains made by Aeroflot in 2023 due to the settlement with aircraft lessors. Those affected both net income and operating results and I took them out. If I hadn’t done that, the gap would have been bigger still.

In any event, I’ve already spent far too long chasing the remaining profit gap. Perhaps the IATA figures make some adjustments to normalise for accounting differences or something. There is certainly plenty of remaining scope for that to be found within the Aeroflot accounts, which I can’t pretend to have fully unravelled. IATA source the data from Airfinance Global and it is behind a pay-wall, so I can’t check properly. If anyone has access and can shed any light, please drop me a message.

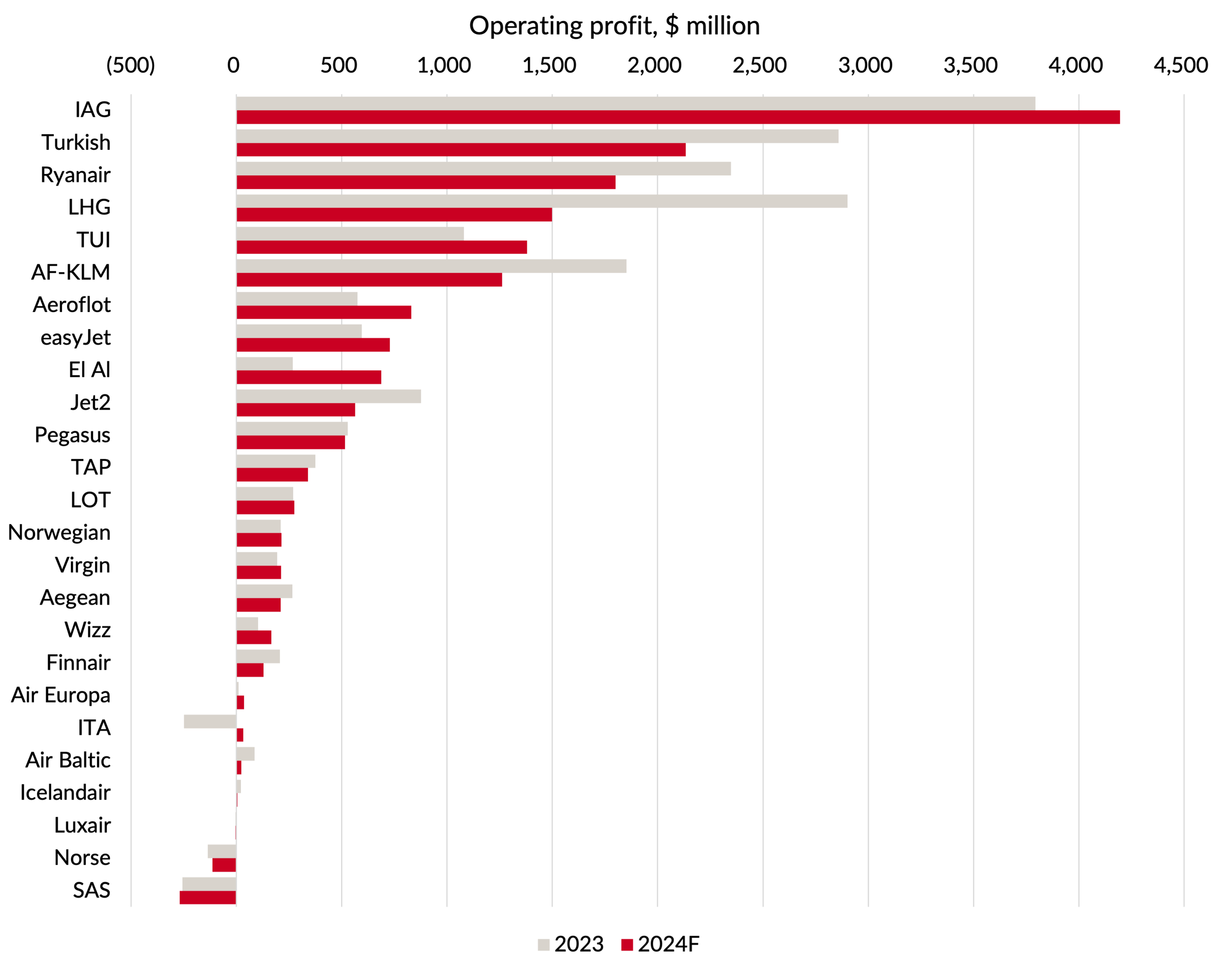

The point of reverse-engineering the IATA numbers is to show how the profit breaks down by carrier and I think we are close enough to be able to do that. The following chart shows the figures for both years, ranked by 2024 forecast profits. Although overall 2024 profits are expected to be lower than 2023, that is far from a consistent story amongst the carriers. Lufthansa Group alone accounts for €1.4 billion of the overall €1.8 billion drop. My rather mechanistic method of estimating 2024 profits results in a forecast operating profit for Lufthansa Group of €1.4 billion, which is at the bottom end of its €1.4 - 1.8 billion guidance. So perhaps it won’t be quite that bad in reality.

Source: Company reports and press releases, GridPoint analysis

It is also interesting to look at the ranking in operating margin terms, which you will find in the chart below, again ranked by 2024 performance. You should note that I truncated the scale on the chart at -10%. That is sufficient to cover almost all the carriers, but not Norse, who somehow managed a -31% margin in 2023 and I still project a truly awful -21% in 2024. At the other extreme, El Al comes out as the surprise (at least to me) likely winner of the 2024 margin crown. In the first nine months of the year they managed a stonking 23.5% margin. They have certainly prospered financially this year as a result of foreign airlines pulling out of the Israeli market due to the war. My forecast of 21% for the full year assumes they replicate last year’s Q4 performance.

Source: Company reports, GridPoint analysis

Post publication note: the 2023 Jet2 figures contain an error on my part (failed to copy a formula!). Thanks to eagle-eyed Matt Newell for pointing this out. The corrected operating profit figure for 2023 (year to September) is $569m, with an 8.4% margin.

Net profit trends

I won’t bore you with all the detail of net profit by airline, since it tells a similar story. I will point out that through a combination of being both very big and very profitable, IAG, Turkish Airlines and Ryanair between them account for more than half (57%) of expected net profits for the European region in 2024.

In the chart below, I’ve shown the various figures for European net profits for 2023, 2024 and IATA’s forecast for 2025.

Source: IATA, GridPoint analysis

The first thing to note is the ~$2.5 billion gap between my estimates and the IATA ones that we talked about earlier (the solid lines). I’ve also shown as dotted lines what IATA published a year ago, and what I thought at the same time (my article from last year is here if you are interested). Last year, I had an even bigger gap in the figures for 2023 ($5.9 billion). Some of that has been closed by revisions to my 2023 figures, including bringing in the additional carriers. More of it has been closed by revisions to IATA’s figures for 2023.

For 2024, we both thought that profits would grow slightly, and whilst that’s proven to be true at IAG and easyJet, performance has been worse than I expected at Lufthansa, AF-KLM and Ryanair.

As far as 2025 is concerned, IATA think that profits will improve a bit, presumably driven by lower fuel costs. We’ll cover that issue in the next section, but I think I would probably agree with that sentiment. I haven’t included my own forecast for next year. Quite frankly, now I’ve seen how dependent the numbers are on the performance of airlines in Eastern Europe which I don’t follow as closely as I do the Western European ones, I’m not sure I’m qualified to comment.

The impact of lower fuel prices

One of the big themes of the IATA report is the impact of lower fuel prices. They assume that jet fuel prices will average $87 in 2025 (based on $75 crude and narrowing crack spreads), down from $99 in 2024, with further cost benefits on top since airlines didn’t fully benefit from lower prices in 2024 due to hedging. 15-25% savings in fuel costs are projected and with industry fuel spend of around $261 billion in 2024, that’s big money.

The flip side of lower fuel prices for airlines is lower ticket prices, as competition forces lower costs to be passed on to customers. IATA estimate that a 10% drop in the fuel price should translate into a 4-5% decline in passenger yields. I have no issue with the assertion that industry-wide cost savings will eventually be passed on in lower prices, but the scale of the effect cited by IATA seems odd to me. With fuel costs representing about 30% of revenue, a 10% change in fuel prices equates to about a 3% change in ticket prices if the effect is going to be profit neutral. IATA seem to be implying that lower fuel prices will lead to lower industry profits, which seems very odd.

Industry capacity growth and supply constraints

IATA do concede that supply constraints will limit the speed at which fuel cost gains will be passed through in lower prices. That’s because the real world mechanism by which airlines end up passing on cost savings is through adding capacity. Lower costs improve the economics of growth. More capacity feeds through into discounting to fill those seats. Supply constraints get in the way of that process, with airlines “forced” to accept higher margins instead.

Many commentators wonder why airlines don’t just constrain growth anyway, if it leads to higher margins. Why do they need an industry supply constraint to do that? The answer of course is anti-trust regulations. Airlines are not allowed to co-ordinate supply volume like OPEC does. Their executives would end up in jail if they tried. The perfect scenario for any airline is where their competitors constrain capacity, but they are free and able to grow themselves. As well as improvements to market share, growth brings unit cost benefits as fixed costs are spread and new hires are made at lower salaries than the average. Growth of your competitors is all bad news. It’s an example of the “prisoner’s dilemma” conundrum from game theory. In the absence of an ability to collude, it is in every airline’s narrow best interest to grow, regardless of what their competitors do. That’s true even if they’d all be better off if nobody did.

SAF and emissions trading costs

This time last year, IATA predicted that global production of Sustainable Aviation Fuel would triple in 2024 to 1.5 million tonnes, although that would still represent only 0.5% of industry fuel volumes. They’ve now updated their estimate of 2024 production to just 1.0 m tonnes, representing a meagre 0.3% of volume. Interestingly, the revision to the percentage is bigger than would be accounted for by the production reduction alone. IATA’s estimate of total fuel use in 2024 has increased by 7%, presumably through some combination of faster capacity growth and a slower pace of replacement of old aircraft due to delivery delays. To state the obvious, the impact on emissions of the faster growth in fuel consumption completely swamps that from the shortfall in SAF volumes.

Source: IATA, GridPoint analysis

IATA continue to forecast rapid growth in SAF production volumes, more than doubling next year. I suspect that this will once again prove to be somewhat optimistic, but the story of rapid growth is undoubtedly correct as new facilities come online and mandates come into effect.

The industry’s global carbon offset scheme, CORSIA, has recently started to drive costs for the industry. IATA published some estimates for the costs of the scheme. For 2024, they gave a range of $460m-$925m and for 2025 $540m-$1,375m. Whilst these are big numbers, even at the upper end of that range, the costs are small in the scheme of aviation’s $261 billion annual fuel bill.

For airlines in Europe, the rising costs of the local emissions trading schemes and the SAF mandates are of much more significance in the short-term. IATA estimated the additional cost of SAF for 2025 will rise to $3.8 billion at an industry level. The cost of the European Emissions Trading Scheme wasn’t quantified by IATA, but if you are interested I wrote about it recently here and it is very meaningful for short-haul carriers in Europe. Whilst the numbers are still relatively small at a global level compared to the total fuel bill, they are quite concentrated on European carriers and airlines will be thankful that the rising costs of SAF and ETS are coinciding with a period of lower fossil fuel prices.

Wishing you a happy New Year

I’m sure that there is much more that I should be commenting on in terms of both the year just finishing and the year ahead. But for once I have a hard deadline to post this article and I’ve run out of time.

Congratulations to the airline management teams that have delivered great results in 2024. For those for whom the year is perhaps one to forget, the good news is that you don’t have too long to wait until it is over.

Wishing you all a prosperous and sustainable New Year.