The growing cost of airline emissions in Europe

European airline profitability - a follow up

My last post looked at the profit performance of Europe’s airlines in 2024 and ended with a few quick comments about the outlook for 2025. One of the things I said was that current fuel prices of around $725 per tonne should be supportive of profitability going into next year.

I was correctly reminded in some of the feedback on that post that the basic cost of fuel was far from the full story these days, with emissions charges expected to rise rapidly, especially for short-haul flights in Europe. So I decided to do a quick follow up post to address the issue. Of course, it didn’t turn out to be quick at all. It is quite a complicated area and one where there is lots of data. Once I started looking into it, I couldn’t resist going down the rabbit hole.

As I did in my previous post on Q3 results, I’m going to focus on the big six Western European airline groups. Whilst they all face the same emissions cost pressures, there are some interesting differences in their situations.

Emissions trading systems in Europe

Airlines flying within Europe have been required to pay for their carbon emissions since 2012, when aviation was included within the European Emissions Trading System (ETS). The ETS is a “cap and trade” scheme that also covers power generation and industry within the European Economic Area (the EU plus Norway, Iceland and Liechtenstein). Switzerland has a linked scheme with mutual recognition of allowances. The cost of the emissions allowances in the EU scheme has varied over the years, typically in the €60-100 range, with recent prices towards the bottom end of that (see chart below).

Pre Brexit, the UK used to be in the EU scheme, but since 2021 it has operated its own scheme. Allowances are not interchangeable and the prices can and have diverged over time, trading at consistently lower prices in recent times.

Source: ICAP, Ember, GridPoint analysis

One of the big questions for airlines is where ETS prices are likely to go in the future. Like any market, that price will be driven by the balance of supply and demand.

The supply side is fully controlled by governments. In deciding how many allowances to create, politicians need to balance two pressures. First there is the desire to cut emissions and ensure that the true economic cost of emissions is levied on the emitters to get the right incentives. From that perspective, the current price is lower than most commentators would see as optimal for driving decarbonisation and meeting climate goals, with figures as high as $200 or even $300 being cited.

On the other hand, driving up the costs of European industry will make it globally uncompetitive if other countries don’t levy the same charges for emissions. Economic activity and the related emissions will just move away from Europe, costing jobs, hurting European economies and potentially increasing overall emissions if energy intensive industries just relocate to less regulated parts of the world.

Between 2021 and 2023, the supply of credits reduced at 2.2% a year, but the annual reduction was increased to 4.2% from 2024 and will increase again to 4.4% from 2028. We’ve already seen that despite the faster pace of reductions in supply this year, the price of credits actually fell. Faster than expected shifts to renewable energy more than offset the increases from the aviation industry bouncing back after COVID. Airline emissions only made up only 3.4% of the total covered by the scheme in 2023, so airline demand doesn’t play a big part in driving the price.

So why the headline about rising costs?

If the price of ETS credits has been going down in 2024, why is this article about rising costs?

Well, the first point is that the airlines which do provide figures are in fact reporting substantial increases in emissions costs in 2024. Air France - KLM spent €203m in the first 9 months of 2024, a 37% increase on 2023. IAG spent €251m, up 39%. Both airlines lock in their emissions credits in advance and they obviously did so at prices which now look high with the benefit of hindsight.

Cost increases at the moment are being driven by volume effects. Airlines can cover part of their emissions with free allowances, but any growth requires them to pay for additional allowances. For an airline which gets free allowances covering half its requirement, a 10% increase in flying will generate a 20% increase in ETS costs.

The free allowances are also being phased out. That started in 2024 in the EU and Switzerland, with 25% of free allowances already eliminated for 2024, rising to 50% in 2025 and free allowances ending in 2026. The UK phase-out won’t start until 2026, but that could even be delayed until 2027 to align with the introduction of the UK Carbon Border Adjustment Mechanism.

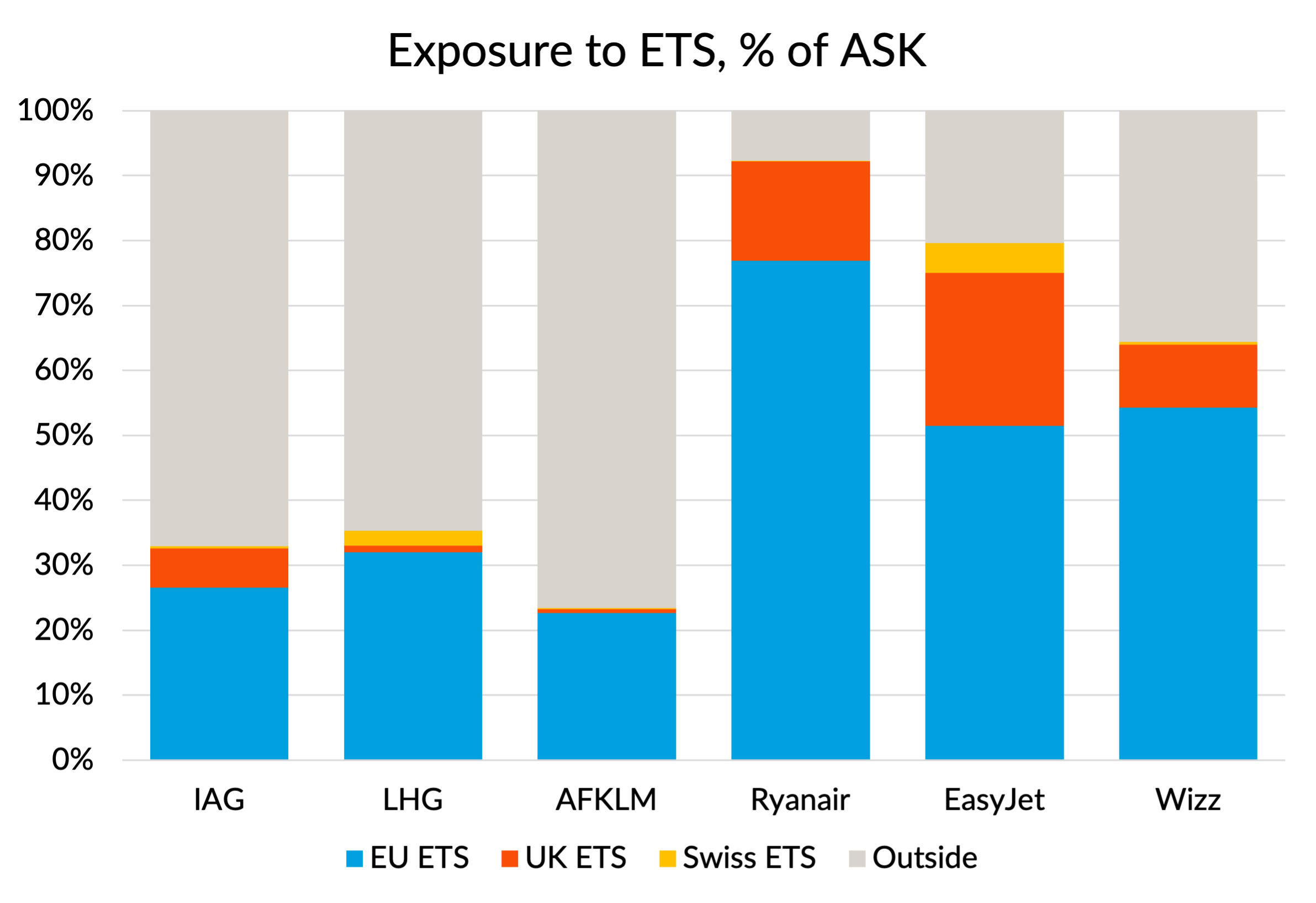

Different airlines are in different positions regarding their exposure to rising ETS costs. The first reason is that currently only flights that are fully within the EEA/UK/Switzerland zone are covered. A flight which departs from the zone but doesn’t land there is not covered. There is a separate CORSIA scheme which levies emissions charges on those flights, but the cost of CORSIA credits is currently a fraction of ETS prices. I’ve shown below the ETS exposure of the big six Western European airline groups, measured by capacity. Ryanair is the most exposed, with almost all its flights taking place within one of the ETS areas.

Source: GridPoint analysis of published schedule data for 2023

Even for flights within the zone, the groups are in different positions when it comes to the proportion of their emissions that are covered by free allowances. The chart below shows the figures for the big six in 2023. I’ve also shown the positions of the constituent group airlines as lighter colour bars.

There are a couple of reasons for the differences. The first relates to the way the initial free allocations were set. That was done using a standard figure of 0.6422 allowances per tonne kilometre flown in the base year, 2010. Airlines which were “more efficient” in terms of emissions per tonne kilometre got more of their initial emissions covered. The second factor driving differences today is how much the airlines have grown since the 2010 baseline. Airlines like Aer Lingus, Swiss and Air France which have not grown much since then were still able to cover a large proportion of their flights with free allowances. Fast growing airlines like Wizz that are much bigger than they were back in 2010 are already paying for more of their emissions and so have proportionately less to lose from free allowances being phased out.

Source: EU and UK government published ETS data and GridPoint analysis

How much money is at stake?

In the chart below, I’ve shown the monetary value of the 2023 free allowances, using average ETS market prices for that year. In absolute terms, Ryanair will be the biggest loser from phasing out these free allowances. We saw earlier that it is the most exposed to the ETS zone, with more than 90% of its capacity covered. IAG is next, despite having a lot of flights outside the zone. It has a bigger short-haul footprint than AF-KLM, for example. For its size, easyJet also looks quite exposed. It has a big footprint in Switzerland, where the baseline was set much more recently, in 2018. It also hasn’t grown anywhere near as fast as Ryanair or Wizz in recent years. The fact that the UK is phasing out free allowances on a slower schedule has obvious benefits to IAG, easyJet and to a lesser extent Ryanair, whilst the full impact will be felt much more quickly by LHG, AF-KLM and Wizz.

Source: EU and UK published ETS data and GridPoint analysis

What happens if ETS prices rise further?

The increased ETS costs shown above only reflect the incremental effect of withdrawing the free allowances at 2023 ETS prices. There is of course also potential for costs to rise further if prices go up.

The UK government publishes scenarios for future UK ETS prices as part of its own cost-benefit analysis for policy development. Prices for 2030, translated into €, range from €104 to €142. For an airline like Ryanair, already facing an increase in costs of €334m from the phasing out of free allowances, a €142 emissions price would take the total cost increase to €1.1 billion, even before the effect of growth. Ryanair’s total revenue in 2023 was €13.1 billion, so covering that through higher prices on its flights in the ETS zone would require around a 9% increase in total revenue per passenger.

Will increased emissions costs get passed on in higher prices?

A cost increase which affects all competitors equally has a good chance of being passed on to customers. But that won’t be without consequences for demand, so it will have an impact on profits, especially in the short-term as the market adjusts. Some carriers may choose to absorb some of the increased costs in lower margins, if they want to apply pressure to competitors who are less able to do the same.

I’ll also point out that as we’ve seen, not all competitors are being affected equally. The price rise required for Aer Lingus to offset the loss of free allowances will be much bigger than it is for Wizz. For the network carriers, a sizeable chunk of their ETS zone capacity is used to feed their long-haul services. To the extent that they are competing only with each other, they might be able to pass the cost on in higher long-haul prices. But they are also competing with carriers operating hubs outside the ETS zone, whose feeder flights from Europe don’t face the same emissions costs.

Other emissions cost risks

As well as the known increases in emissions costs, there are also some scarier scenarios for airlines, their customers and their investors. For example, flights which are not covered by the ETS today may over time have to pay similar emissions costs, either through the cost of the CORSIA scheme rising to similar levels or an expansion of the scope of ETS.

The price of credits could also be higher than the scenarios illustrated above. As I said earlier, some analysts put the “true” social cost of CO2 emissions at much higher levels. Another reference point is what airlines are using to stress test future scenarios. IAG discloses the assumptions it uses when testing the carrying value of its airline subsidiaries, with €173 as an assumption for the value of ETS allowances in both the EU and UK schemes.

The EU is looking into the question of levying emissions charges on airlines for non-CO2 climate effects such as contrails. If those costs do get incorporated, that could easily double the cost of the scheme.

Sustainable Aviation Fuel (SAF)

On top of the direct emissions costs, airlines in Europe also face the cost of SAF mandates in the EU and UK from next year. Initially, fuel suppliers will be required to blend SAF at 2%, rising to 6% by 2030 in the EU and 10% in the UK. With SAF costing at least double fossil kerosene prices and likely to be in short supply, even a 2% blending mandate will add hundreds of millions of euros to airline costs.

The ETS rules allow emissions to be adjusted down for the use of SAF. A tonne of SAF might cost the airline a premium of $1,500 or more, but with an ETS price of say $100, it will directly save $315 of ETS costs (each tonne of fuel produces 3.15 tonnes of CO2). The EU has also created a pot of additional free allowances which are available on a “first come first serve” basis to help bridge the extra costs of SAF. Quite how that will work in practice isn’t clear to me, but I guess it will help a bit.

To estimate the potential additional costs to airlines from SAF mandates, we can look to figures reported by Air France - KLM, one of the leaders in terms of SAF adoption and the only airline to my knowledge who splits out the extra costs of SAF. In the first nine months of 2024, the additional costs to them of sourcing SAF amounted to €166m, an increase of €60m on the prior year. Scale that up to a full year and to the size of all six of these six groups and you’d get a figure of over a €1 billion of additional costs. And remember that these costs are based on AF-KLM’s costs in 2024, before the introduction of the SAF blending mandates.

Strategic implications

A billion here, a billion there. Pretty soon you are talking real money that could have strategic implications. I don’t have time to explore all of these, but I’ll touch on a few.

The first thing I’ll say is that any emissions costs which are levied on a “level playing field” basis are equivalent from a strategic perspective to an increase in the fuel price. Even a $100 per tonne of CO2 levy is the equivalent of “only” a $300 increase in the fuel price, or $30 a barrel of crude. That’s big, but not outside the kinds of swings in oil prices the industry regularly battles its way through. Adjusting to such an increase in costs can be very painful, but when a cost increase hits everybody it will in time be passed on to consumers in prices. There will be an impact on demand of course, and so total capacity will need to be lower if prices need to be higher. Getting to a new equilibrium can be something of a bumpy ride. Everybody would prefer their competitors to do the capacity adjustment and to maintain their own plans. It will be the airlines with better margins and stronger balance sheets that will have the luxury of choosing their own path.

All other things being equal, rising emissions costs will tend to favour airlines with the most fuel-efficient aircraft. But having the lowest emissions per passenger kilometre doesn’t guarantee that you’ll be a winner. If prices are going to have to go up, the price sensitivity of your customers also matters a lot. High seating density is great for emissions per passenger, but tends to be correlated with an extremely price sensitive customer base. Corporate customers, with their own sustainability targets to meet, have proven willing to cover additional sustainability costs if that can be directly linked to reduced emissions.

The obvious winners to me will be airlines located just outside the ETS zones, with Turkish Airlines being a prime example. Whilst they can’t escape the requirement to source SAF in EU markets, being outside the ETS should help them feed their Istanbul hub at much lower cost than airlines with hubs inside the zone, giving a significant competitive advantage.

I’d also expect the more geographically mobile low-cost carriers to prioritise growth outside the ETS boundaries. But even airlines which are anchored to their hubs can review their route network. The attractiveness of destinations outside the zone will increase relative to those within it.

Finally, airlines who are able to lock in supplies of SAF at lower prices than their competitors may be able to secure a competitive edge, in a way that has not really been possible for fossil fuel costs. The bigger, better funded airlines will be helped by having balance sheets capable of standing behind long-term off-take agreements. Investing in SAF suppliers and projects has also been an important mechanism for securing preferential access to supplies. But being big is, as always, no guarantee of success. It is still early days in the development of the SAF industry, with plenty of scope for smart strategies to make a difference. Being nimble and willing to experiment and take some risks is likely be at least as important a factor as scale.

Outlook for profitability

Am I still cautiously optimistic about European airline profitability for next year? I think so.

But I will admit that a lot is riding on the ability of airlines to keep passing on increased costs to customers. If economic conditions turn against the industry or customers rebel, cost cutting and right-sizing are going to be back on the agenda.