Full year 2024 results from Heathrow

Record profit before tax, despite lower airport fees

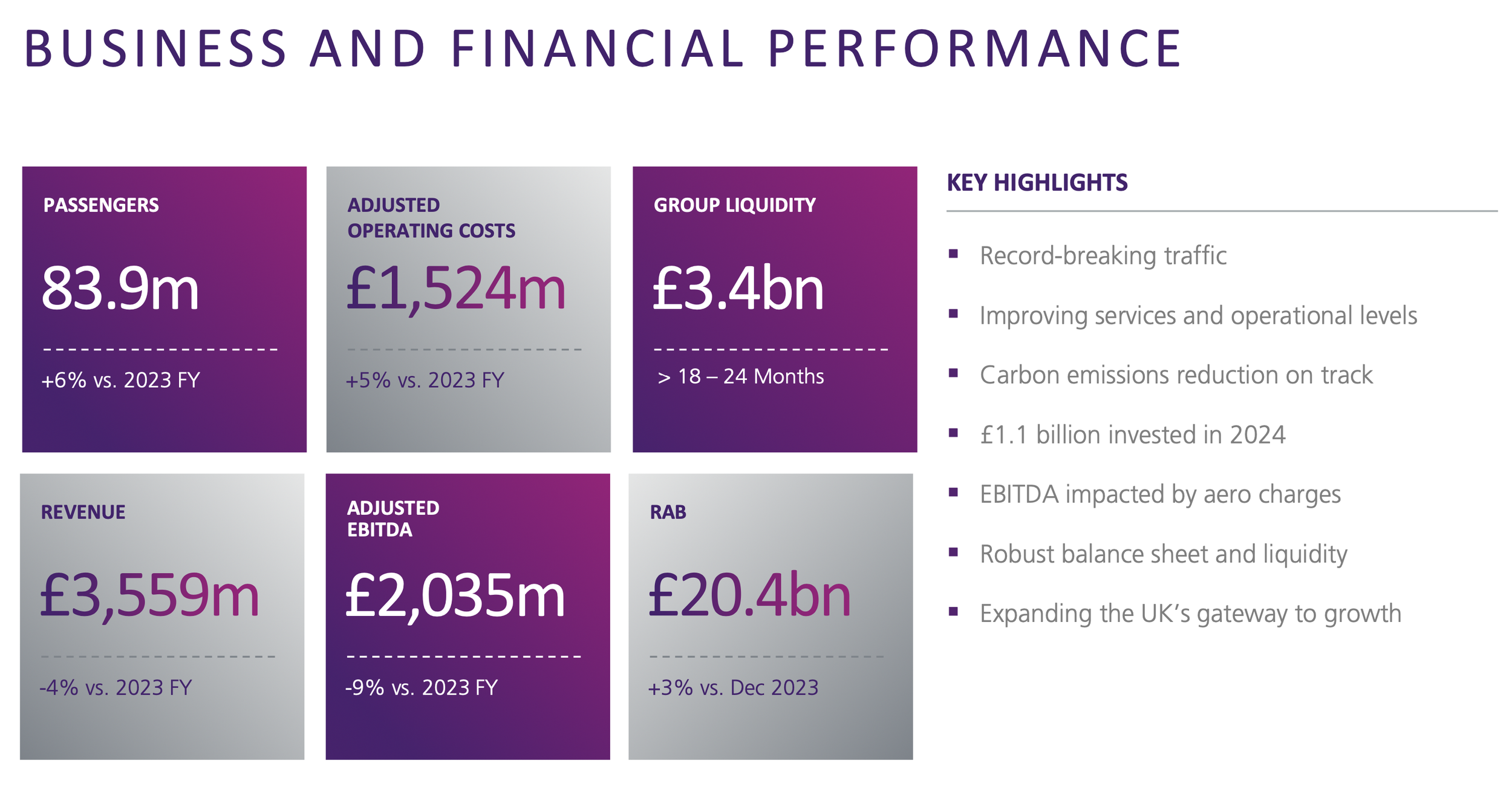

Pre-tax profits at Heathrow for the full year 2024 rose 31% to a new record of £917m. That was achieved despite a reduction in regulated airport charges of 14%, something that the company had been warning would lead to dire financial consequences. In their results presentation, the airport’s management tried their best to focus on the negatives, with “Adjusted EBITDA” the only profit metric which made it to their “highlights” slide (shown above). That measure was down 9% on the previous year.

The figure for profit before tax could of course be found In their press release, accompanied by their preferred “adjusted” figure, which was lower at £450m. The adjustments they make are mainly to exclude volatile “mark to market” items related to the complex financial derivatives the airport employs. Leaving them out is supposed to smooth out some of the volatility and, as you can see from the following chart, the adjusted figures are a little smoother. But they have also been consistently below the unadjusted figures over the last two years. A cynic might wonder if there is another motive for focusing on the adjusted figure.

Versus last year, adjusted profit before tax was up by £412m, an even bigger improvement than we saw for the unadjusted figure. In their table of results, Heathrow gave the percentage change versus last year as “N/A”. I suppose they thought reporting a 1084% increase in profits wouldn’t fit their narrative.

Source: Company reports, GridPoint analysis

As I’ve already said, this was a record-breaking pre-tax profit result, building on last year’s results which were also a record. The following chart shows the profit history of Heathrow for the entire period since BAA was broken up. You can see how much stronger the post-pandemic profits have been compared to the pre-pandemic period.

Source: Company reports, GridPoint analysis

How did I do with my own profit forecast?

When Heathrow reported its results for 2023 a year ago, I had a go at working out how badly Heathrow would be impacted by the CAA’s reduction in airport charges. The airport’s results are very sensitive to volumes, so the most important assumption is the passenger forecast. In the chart below, I’ve shown my forecasts in yellow and I’ve also shown Heathrow’s official forecast. In both cases I’ve shown how those estimates developed during the year.

I’ve pointed out many times before how “low-balled” the airports public forecasts always are, so it is not a surprise that the actual outturn of 83.9 handily beat their forecast. But in fact passenger numbers came out even better than my own estimates.

Source: Company reports, GridPoint analysis

On the basis of my start of the year passenger forecast of 82.7m, I thought that operating profits would fall by £200-300m compared to 2023. I didn’t give an explicit forecast for EBITDA, but applying that same £200-300m reduction would give a range of £1,928-2,028m. Even the low end of that range was substantially above the airport’s own guidance from December 2023 of £1,885m.

As the airport was forced to slowly increase their passenger forecast during the year, they did also increase their profit guidance. But the final result of £2,035m was £72m better than their guidance from as recently as December, when they would have known the actual passenger numbers for the year.

The final result was slightly above the top end of my range, essentially driven by the better volume outturn. Operating profits fell by £209m, just squeaking into my £200-300m range.

Source: Company reports, GridPoint analysis

Dividends resumed

One of the points of contention with airlines has been the amount of dividends paid out to Heathrow’s shareholders over the years, at a time when the airport’s charges were amongst the highest in the world and management was still pushing hard for further increases.

Dividends were suspended when the pandemic hit. Despite the profit rebound since then, the company has been cagey about when they might resume. In their June investor report they said:

“No dividends are currently forecast for 2024, although it is plausible subject to financial performance”

Although the topic wasn’t mentioned in their December report, it had been clear for some time that they did intend to pay a dividend. According to a filing with Companies House made in August 2024, the company executed “a concurrent bonus issue and capital reduction as part of distributable reserves management”. That was a legal process required to enable them to pay a dividend, despite the fact that the company still had accumulated losses of over £1 billion (in fact, the company’s debts exceed its assets by around £5 billion).

So it came as no surprise to me at least that when the results were announced, a dividend of £250m was declared and it was confirmed that this would be passed up through the multiple levels of holding companies and paid out to the ultimate shareholders. I guess that reduction to airport fees wasn’t quite as unaffordable as they’d made out.

Outlook for 2025 and 2026

I haven’t done any specific estimates for profits this year and next, but the outlook seems relatively benign to me.

Airport charges will rise with inflation each year and although many costs are subject to inflationary pressure, not all of them are. And you would have thought there should be scope for efficiency improvements too.

There is also some small upside to come from further increases in passenger numbers. The scope is limited of course, because now that traffic has fully recovered from the pandemic, the airport is essentially full again. Heathrow thinks passengers will go up by 0.5% in 2025 but, as usual, I think that’s too low. Published capacity is up 1.5% and January volumes were up by 0.93%. So I’d probably plump for a 1% increase. That’s still pretty marginal, but with most of Heathrow’s costs fixed it should still push up margins.

Quite what the outlook is for financing costs is much harder to say, given the complexity of Heathrow’s funding arrangements. Operating cashflow was positive to the tune of over £1 billion in 2024, despite capital expenditure of £937m. Net of interest payments, that still left a surplus of around £500m. As we saw earlier, half of that has been ear-marked for dividend payments to Heathrow’s shareholders, but on the face of it there should be scope to pay down some debt unless capital expenditure rises further. With both debt levels and interest rates falling, financing costs may continue to decline. Taken together with rising operating profits, I think we should be in for another year or two of record pre-tax profits.

Future investment and expansion plans

Heathrow does of course have big capital expenditure plans. The way it is regulated, the more money it spends, the more money it makes. The company values its business assuming a 30% premium to its regulatory asset base (RAB). That calculus means that if it borrows an extra £1 billion and invests it in expanding its RAB, that’s another £300m of value for its shareholders.

For anyone who has been scratching their heads over how a third runway at Heathrow can possibly cost £40 billion or more, that last paragraph might give you a clue.