Will the oil price hike derail the airline recovery?

Just when things were looking up…

Although the pandemic is far from over, for most countries the restrictions that were imposed on travel have been progressively dismantled. In the UK, today was the first day for 21 months when travellers could come to the UK without travel restrictions or testing requirements. China and Hong Kong remain closed and tests are still required to travel to the USA, but airlines in the USA and Europe have been restoring capacity to close to pre-pandemic levels and reporting booking volumes at or above 2019 levels. As predicted by many, pent up demand is driving a strong recovery once restrictions are removed and customers are able to book with confidence.

Those airlines that survived the worst two years in the industry’s history needed a few years of “clear air” to restore their operations, rebuild profitability and pay down the massive debts they took on during the crisis. But they have run straight into another patch of turbulence, triggered by the war in Ukraine. There have been direct impacts, most notably the loss of Russian overflights. But by far the most significant impact has been the rise in the oil price.

Although the jet fuel price has come down a bit from the highest levels it reached, it still remains over 50% higher than at the start of 2022 and 80% higher than this time last year.

Source: IATA

Implications for the recovery

Will the rise in fuel prices kill off the recovery in industry profitability? That depends on whether fuel cost increases can be offset by other cost savings or passed on in higher prices. With airlines having spent the last two years slashing costs to the bone, adjusting to higher fuel costs will mainly have to come through higher prices for customers.

Will airlines have the collective discipline to raise prices? Or will market share wars make that impossible? And if they do manage to raise prices, will that kill off the demand recovery? The answers to those questions are likely to vary by geography due to differences in demand conditions and industry structure.

Let’s start with the USA.

US market

The big three US airlines all presented to JP Morgan’s Industrial Conference earlier this week. They all talked up the strength of the recovery in bookings and expressed confidence that fuel cost increases could and would be quickly passed on to customers in higher prices, without material demand impact.

I’ve picked out two slides from the United Airlines presentation which I think best tell the story of the current strength of bookings. Leisure demand in particular is very strong and overall bookings held by United for future travel are now just 2% below 2019 levels. Since we know that all airlines have seen big shifts towards late booking behaviour, that must mean that near term bookings are significantly above pre-pandemic levels, despite capacity still not having been fully restored.

What about yields? That will be driven by a combination of fare levels and business travel mix. Whilst business travel has been slower to recover than leisure, the US airlines were also seeing a strong recovery coming through there too, with business bookings back to 70% of pre-pandemic levels and continuing to trend upwards. Higher yields in that segment were also helping revenues.

Delta said that unit revenues for the month of March would be in line with 2019. That is measured by TRASM (Traffic Revenue per Available Seat Mile), capturing the combined effect of load factors and average prices.

They expressed full confidence that the increase in the fuel price could be passed on in higher prices. With all the major airlines unhedged for fuel, they gave a figure for what that would take in terms of price rises. Relative to an average fare level of $200, they said it would need a $15-20 increase, so 7.5-10%. Shorter booking lead times would enable higher selling prices to feed rapidly into flown revenue, with the increased fuel prices being fully offset by yield increases as early as Q2.

Consolidation in the US over the last few years means that the big 3 command a big percentage of the market. Crucially, they are also all roughly equally sized, and so the competitive environment is quite “stable”. Below is a slide shown by American Airlines making this point. It is more important for these three to see market prices rise than to try and steal a march on each other. All the airlines were keen to emphasis to investors that profitability was the main priority, not market share.

With all three raising prices to offset fuel cost increases, those prices will probably stick from a competitive point of view. The main question mark is how much higher prices will impact on demand. The airlines were playing down any impact, although they signalled their willingness to trim capacity if necessary.

Economists would answer this question by applying a demand elasticity. For intra-US demand, that has been estimated by IATA at -0.6. So a 10% increase in prices would be expected to reduce demand by 6%. In normal times, that would be a significant change requiring a big adjustment to capacity, but given the extreme volatility of passenger numbers in the last two years, it almost seems like something of a rounding error these days. Certainly, the US carriers believe that the demand environment is strong enough to absorb a big price increase with minimal capacity adjustments.

What about Europe. Will things be different there?

Europe

The recovery in demand in Europe has been lagging the USA and the recovery is therefore less firmly established. However, with travel restrictions within Europe now largely dismantled, the same fundamentals should apply in Europe too. If anything, pent up demand should be an even bigger factor as demand has been suppressed for longer.

In terms of the cost increase that needs to be offset, European carriers have an even bigger challenge to deal with due to the weakening of the euro against the dollar. That will push up both fuel costs and other dollar denominated costs like aircraft leases and most maintenance costs.

On the other hand, airlines in Europe take a different approach to fuel hedging. For the second quarter, European airlines have typically hedged 65-75% of their fuel costs. In theory, fuel hedges shouldn’t alter pricing or capacity decisions. The loss or gain on a hedging portfolio depends only on the price, not the volume of fuel consumed. A tonne of fuel saved at the margin will reduce costs at the spot price, regardless of the level of hedging. That means that real world decisions should be driven by the spot price, not the hedged price. But I know from experience that this isn’t the way airlines actually think and behave. Hedging gains reduce the financial pressure to raise prices in the short term and will act to slow down both the financial impact and the pricing / capacity response.

The other big difference between Europe and the USA is the level of concentration in the market. For intercontinental routes, the European players have an even firmer grip on intercontinental capacity than their US counterparts. But for intra-European flights, the big three network airline groups in Europe don’t have anything like the market share that the majors enjoy in the US domestic market. Market share positions are also not stable because in the intra European market, the biggest player is Ryanair and they’ve made it clear that market share gains are a key goal.

Working out how Ryanair will respond to the fuel price increase is therefore critical.

The Ryanair factor

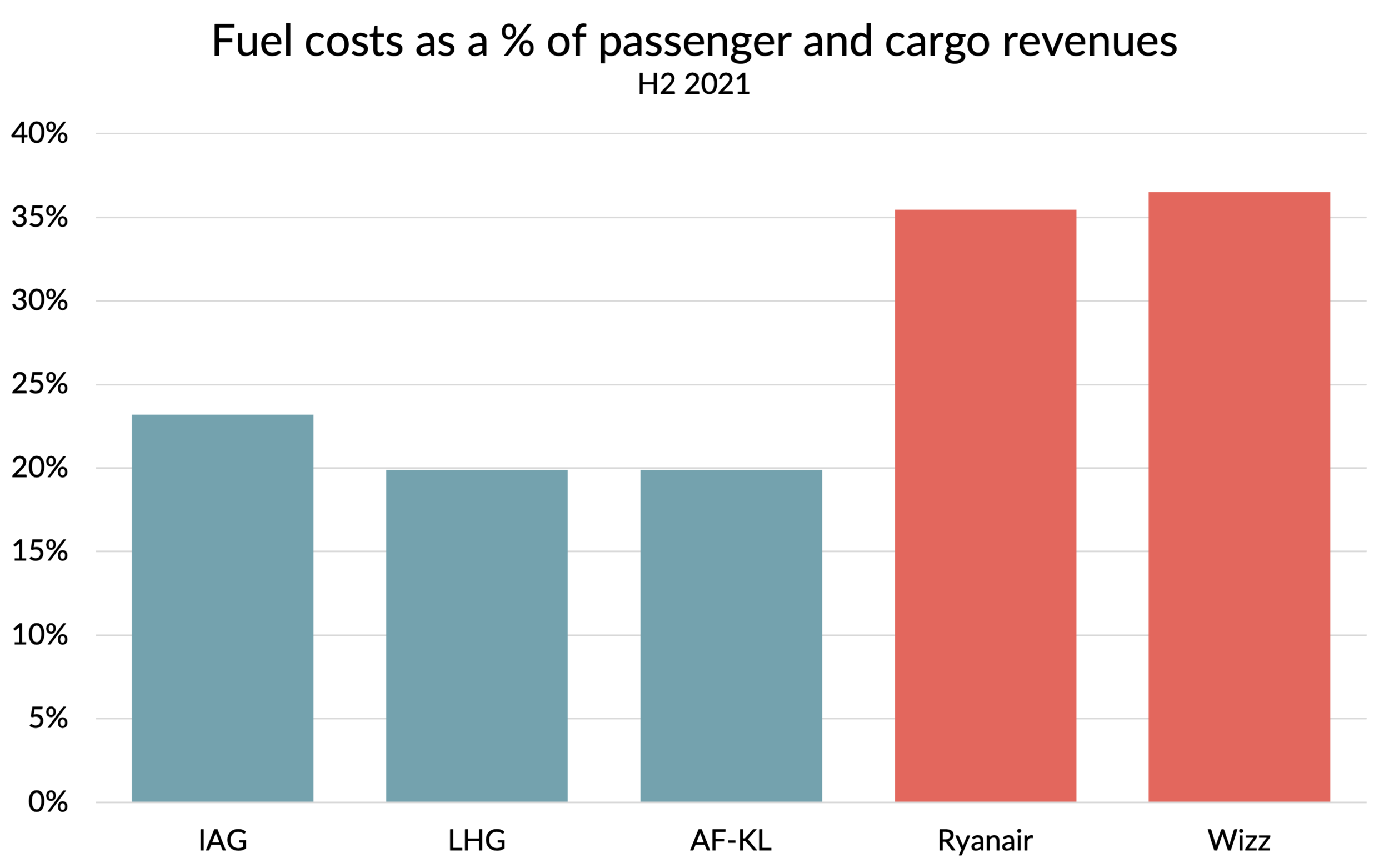

On the face of it, Ryanair should be even more highly motivated to raise prices. Fuel makes up an even bigger proportion of costs for Ryanair than it does for the network carriers. In the second half of 2021, fuel costs represented 35% of revenue at Ryanair (and at Wizz), compared to around 20% at the network airline groups.

Source: Company reports, GridPoint analysis

For all that the low cost carriers shout about their fuel costs per passenger being lower than the network carriers due to younger, more fuel efficient aircraft, higher seating densities, and higher load factors, the fact remains that to offset a given increase in the fuel price, the low-cost airlines will have to increase prices by a much bigger percentage.

Given that they have the most price sensitive customers, that creates a big dilemma. Raising prices is quite likely to be revenue negative for them, as the volume loss will outweigh the benefit of the price increase. To get a positive profit impact from a price rise will therefore require capacity cuts. That’s something that they would probably do in the off-peak winter season, but will be reluctant to do this summer. Their ability to sustain market share gains made during the pandemic is a big part of their story to investors.

Ryanair is the most heavily hedged of all the European airlines, with 80% of their fuel costs locked in. If they want to, that will allow them to maintain their capacity, keep prices low and pile the pressure on their less heavily hedged competitors. They would make more money in the short term if they raised prices and adjusted capacity down, but they don’t need to and I don’t think they will for strategic reasons.

The “Ryanair factor” is going to make it hard for other airlines to raise prices without seeing a big hit to demand. If they do it anyway and just cut more capacity to absorb the volume loss, they will be ceding even more market share to Ryanair. It’s going to be a tough few months as this shakes out, with the unhedged Wizz looking particularly vulnerable.

For the network carriers, balance sheet strength and strategic determination will be decisive in determining whether the fuel price spike results in yet more ceding of market share to the already dominant Ryanair. We’ve seen from recent events in Ukraine what happens if you keep giving ground to a bully, however rational that might be in the short-term.

Long-haul to the rescue?

Since the pandemic started, exposure to long-haul routes has been a big financial drain on airlines. Those routes were the hardest hit by travel restrictions and have been the slowest to recover. But that’s been changing in recent weeks as long-haul markets have reopened and bookings have come surging back.

The long-haul market from Europe is much more concentrated, with most of the capacity in the hands of three big alliance groupings who co-ordinate capacity and pricing. I’m much more confident that fuel price increases will get passed through into prices there. That should translate into a big rebound in profitability, which will provide much needed cashflow.

A tricky few months ahead

Like the real war going on in Ukraine, the battle for market share in the intra European market this year is likely to be drawn out and bloody. But if oil prices remain high into the winter season, Ryanair will eventually be forced to raise prices and adjust capacity as its hedging unwinds.

The network carriers will be praying that a return of long-haul profits will provide them with the financial firepower to hold the line until the oil price recedes or Ryanair’s hedges run out.

Some management teams won’t have the stomach for the fight, and some may lack the financial resources or the backing from their shareholders to fight even if they want to. But wherever Michael O’Leary senses weakness or a lack of commitment, he’ll push harder.

Time perhaps for airline leaders in Europe to take some inspiration from President Zelenskyy and stand their ground in the face of aggression.