Predictions for 2022

Time to roll the dice again

Last year, boutique executive search firm Venari Partners asked me to write about what I expected the new year to hold for the travel industry, and they’ve asked me to do the same again this year.

Only four days after I published last year’s article, news broke about the discovery of Alpha, the first of the new super-spreading variants. I’m hoping that we’ve already had this year’s end-of-year shock development, with the arrival of Omicron.

In many ways, the end of 2021 seems uncannily like the end of 2020. We have a new variant, which spreads much more rapidly. Governments are imposing travel bans on countries where the new variant has been identified. Amidst rapidly rising cases, lock-downs loom and travel company share prices are slumping again.

Will 2022 be as bad for travel as 2021 turned out to be? And if it is, how could travel companies survive another “lost year”? That depends on developments in the pandemic, but also critically on government policy responses to it. That makes it doubly hard to predict and with so much uncertainty, it is worth exploring both the optimistic and the pessimistic scenarios.

Before I do that, let me start with a couple of things that seem likely to hold true whatever happens with the pandemic.

No shortage of underlying demand

A year ago, we didn’t really know whether travellers would return once travel restrictions were lifted. I think we are now quite confident that they will. Every time that restrictions were lifted in 2021 and travellers felt that they could book with confidence, demand came roaring back. The longer this goes on, the more true that is, I think.

The only remaining question perhaps is over business travel. We know that companies have cut travel budgets and the sustainability agenda is a bigger factor than it was two years ago. Some predict that business travel will be halved compared to pre-pandemic levels, whilst others are much more optimistic. IAG’s CEO Luis Gallego, believes that a recovery to 85% of 2019 levels is a “conservative assumption”. For myself, I’m closer to Luis’ view, but I don’t think it will be that good in 2022.

Limited capacity for more debt

According to IATA, the airline industry worldwide will have racked up losses of $190 billion during 2020 and 2021. That’s despite $130 billion of wage subsidies, equity injections and direct, non-refundable assistance from governments. Without those, losses would have been far greater.

Source: IATA, October 2021

The losses have been funded in part by around $100 billion of government loans and loan guarantees, plus another $10 billion or so of other refundable assistance such as tax deferrals. Whilst some private sector equity has been raised, most of the rest has been funded by additional private sector debt. All of that will need to be repaid.

In 2019, the industry made profits of $26 billion. Even if it immediately bounced back to pre-COVID levels of profitability in 2022 and 100% of profits were used to pay back debt, just paying back the government and government-backed debt would take until the end of 2025. In fact, IATA’s forecast for 2022, done before Omicron, was for another $12 billion of losses in 2022. If that worsens to anything approaching 2021’s $52 billion, that would extend repayment timescales out to 2028.

There are a few airlines which still have unused debt capacity and some could raise additional equity capital from the private markets, but for almost everyone in the industry, the scope to take on additional borrowings has been exhausted. 2022 needs to be cash positive at an operating level.

If that doesn’t happen, many will be pushed into defaulting on their debts, unless governments come to their aid.

The pessimistic scenario

The first couple of months of 2022 at least will be very difficult for airlines. Never a good time of year, even in normal market conditions, the Omicron variant and the travel restrictions that governments have introduced in response have already make it worse.

This is usually a peak time of year for bookings. As well as being important for profitability later in the year, those bookings should be bringing in much needed cash. It is easy to see a scenario where the confidence of travellers, investors and lenders all come under massive pressure. One or two big failures could trigger that. Like a run on a bank, a loss of confidence can be self-reinforcing.

In this scenario, governments would need to step in again. The “benign” version of this for the industry would be for governments to step back from travel restrictions and start acting to build confidence amongst customers and investors. Like they would if the financial system came under similar pressures.

Unfortunately, an individual country cannot achieve this by themselves. Travel requires borders to be open at both ends, so international co-ordination is required. Thus far, that has been sadly lacking. Politicians have instead tended to treat restrictions on foreign travel as an easy option when they need to be seen to be doing something.

If confidence is lost, governments will be faced with a difficult choice. To let airlines and other travel companies fail, or to step in with financial assistance. Not loans this time, but money that doesn’t need to be repaid. There will be a temptation for this to be “targeted” at the weaker companies - those most in need of help. That would be cheaper for governments in the short-term, but would come at a great cost in terms of market distortions and will prompt legal challenges from stronger competitors. Better in my view for governments to provide neutral assistance, like extending salary subsidies, tax cuts or direct compensation for the impact of restrictions.

For me, the worst of all scenarios for the industry would be one where government responses vary widely, with some stepping in to help airlines and others letting them fail. A strategy by some but not all countries to “let the market decide” could lead to an industry where politics not economics decides the future shape of the industry. After all the progress made over the last 20-30 years to depoliticise the industry, that would be a tragedy.

The optimistic scenario

If you have made it this far without heading off to drown your sorrows, I can reassure you that this post will get more optimistic from now on.

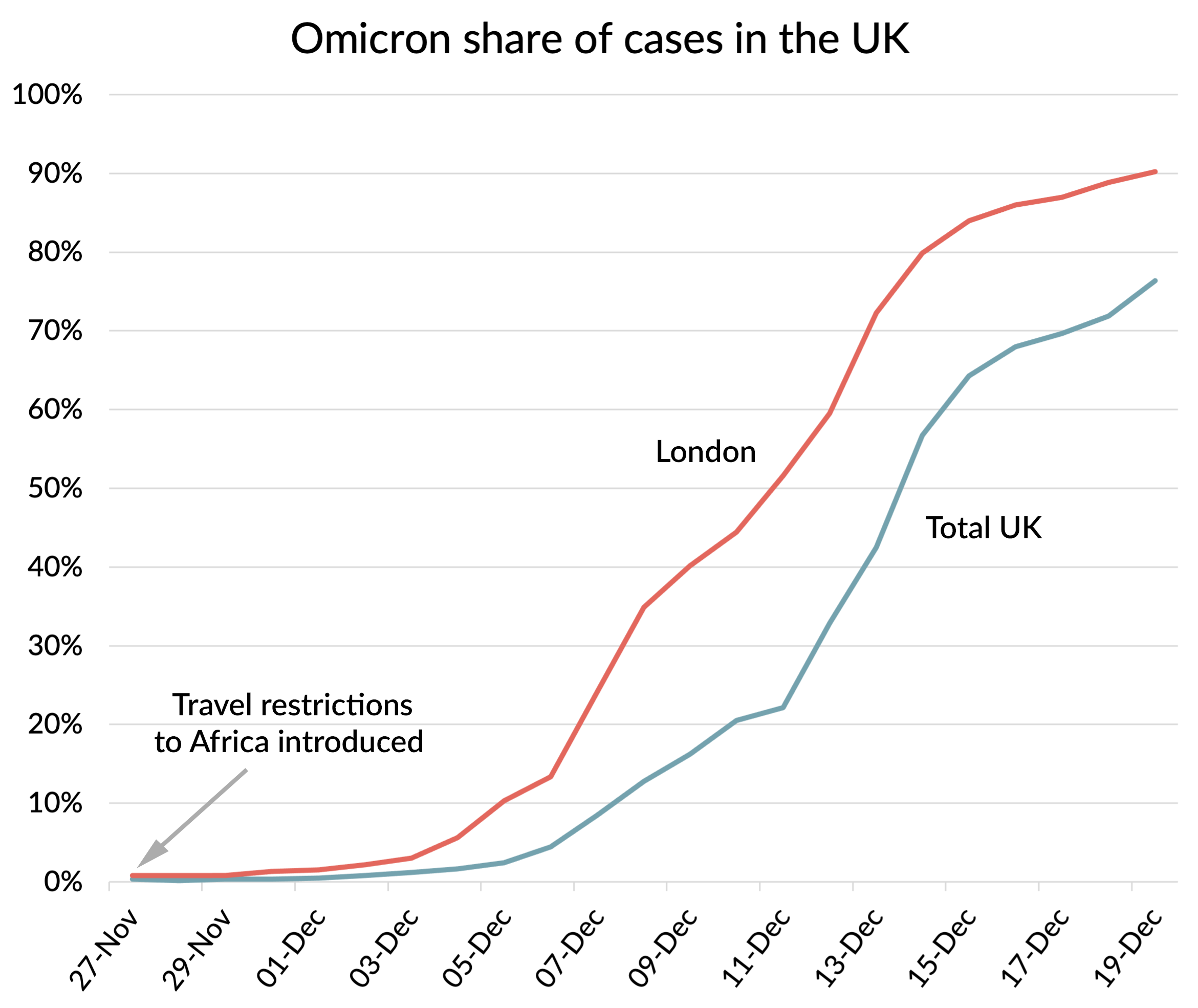

As I pointed out in an earlier article, I think that Omicron related travel restrictions will end up being very short-lived. The sheer speed at which it has spread around the world is quite astonishing. Since South Africa alerted the world to the new variant at the end of November, it has taken less than a month for Omicron to become the dominant strain in Europe and the USA. That’s despite countries moving very rapidly to restrict travel from large parts of Africa. That probably slowed down the virus by a few days. The UK has some of the best data on variant spread in the world and only a week after travel restrictions were imposed, cases were clearly rising exponentially. Over 90% of cases in London are now Omicron.

Source: UKHSA, Omicron daily overview: 22 December 2021. Number of cases with SGTF by day.

The Omicron wave is going to be very sharp. Nobody knows whether it will overwhelm health systems or not, but there are reasons for optimism. In both South Africa and the UK, we’ve seen a drop in the average severity of cases with Omicron compared to previous waves. According to recent studies published in the UK, some of this appears to be due to Omicron being intrinsically a bit less severe (circa 30%). But more importantly, a big part of the reason Omicron is spreading faster is that immunity from prior infection or vaccination is less effective in preventing infections than it was for Delta. In a population with high levels of immunity, very many of the new Omicron cases are therefore reinfections or “vaccine breakthrough” infections. The protection against severe outcomes from vaccines or prior infection is holding up pretty well against Omicron, so these people are much less likely to get seriously ill than the average Delta case.

The drop in average severity per case could still be overwhelmed by the sheer number of cases, of course, given how rapidly Omicron is spreading. That fear is driving a ramp up in domestic restrictions. However, whatever happens, the speed and height of the Omicron tsunami will also mean that it begins to subside again all the sooner, as the virus runs out of people to infect.

It is perhaps ironic that the sheer speed of spread of Omicron could be helpful for the travel industry. It will shorten the time when countries restrict travel, hoping against prior experience that the new variant can be kept out, or at least slow down its arrival. Omicron has demonstrated like nothing else ever could how little travel restrictions do to limit the spread, unless a country seals its borders to the whole world on an essentially permanent basis. We’ve seen that countries can’t react fast enough to stop the arrival of new variants even when surveillance systems are in place. There was no “signal” from the UK’s much vaunted arrivals testing programme that triggered action on travel from South Africa. The move to restrict travel and impose quarantine came in response to reports from South Africa itself and whilst those were admirably timely, they still came too late.

Travel restrictions can perhaps slow down the spread of new variants, but the benefit seems pretty marginal compared to the significant costs. That has always been the position of the World Health Organisation, but it hasn’t been a politically acceptable position for leaders to take up to now during the pandemic.

With their citizens rebelling against restrictions and what I think will be a clear demonstration from Omicron that travel restrictions achieve very little at great cost, I’m hopeful that 2022 will be the year that governments move away from such knee-jerk responses, even if we do get more COVID variants emerging during the year.

Hoping for a better 2022

However bad the first quarter of 2022 will turn out to be, I’m pretty sure it will be substantially better than 2021 was, at least in the UK and Europe. Remember that non-essential overseas travel was literally illegal for UK citizens until the end of May.

I expect the additional testing requirements introduced by the UK in response to Omicron to be relaxed again fairly early on in 2022. The same should be true for travel restrictions being imposed by other countries, as they all inevitably fall to the all-conquering Omicron variant and accept that limiting imported cases is low-impact / high-cost once domestic transmission has taken hold.

Whether this will happen fast enough to save the ski-season is perhaps a 50/50 bet (I’ll admit to having a personal dog in this race). But Easter should be strong and I think the summer season in the Northern hemisphere will be the first “normal” season for three years. Pent up demand could even make it one of the strongest in years.

Of course, this could all be blown off course by the emergence of a substantially more lethal variant. But then the Earth could be hit by an asteroid too.

Sorry, I promised that this post would get more optimistic. Pass the bottle.