War in Europe

A dark day

I’m sure that like me, you’ve spent much of the day watching the terrible news from Ukraine. On days like these, it is hard even to absorb the news and even harder to think about the practical implications. But I know that airline management teams across Europe will have been forced to do just that and I felt the need to give it some thought myself.

Share price drops

I know that stock market prices might be seen as the least important thing today. But they do tend to encapsulate an overall view of the significance of the event, so I am going to start here.

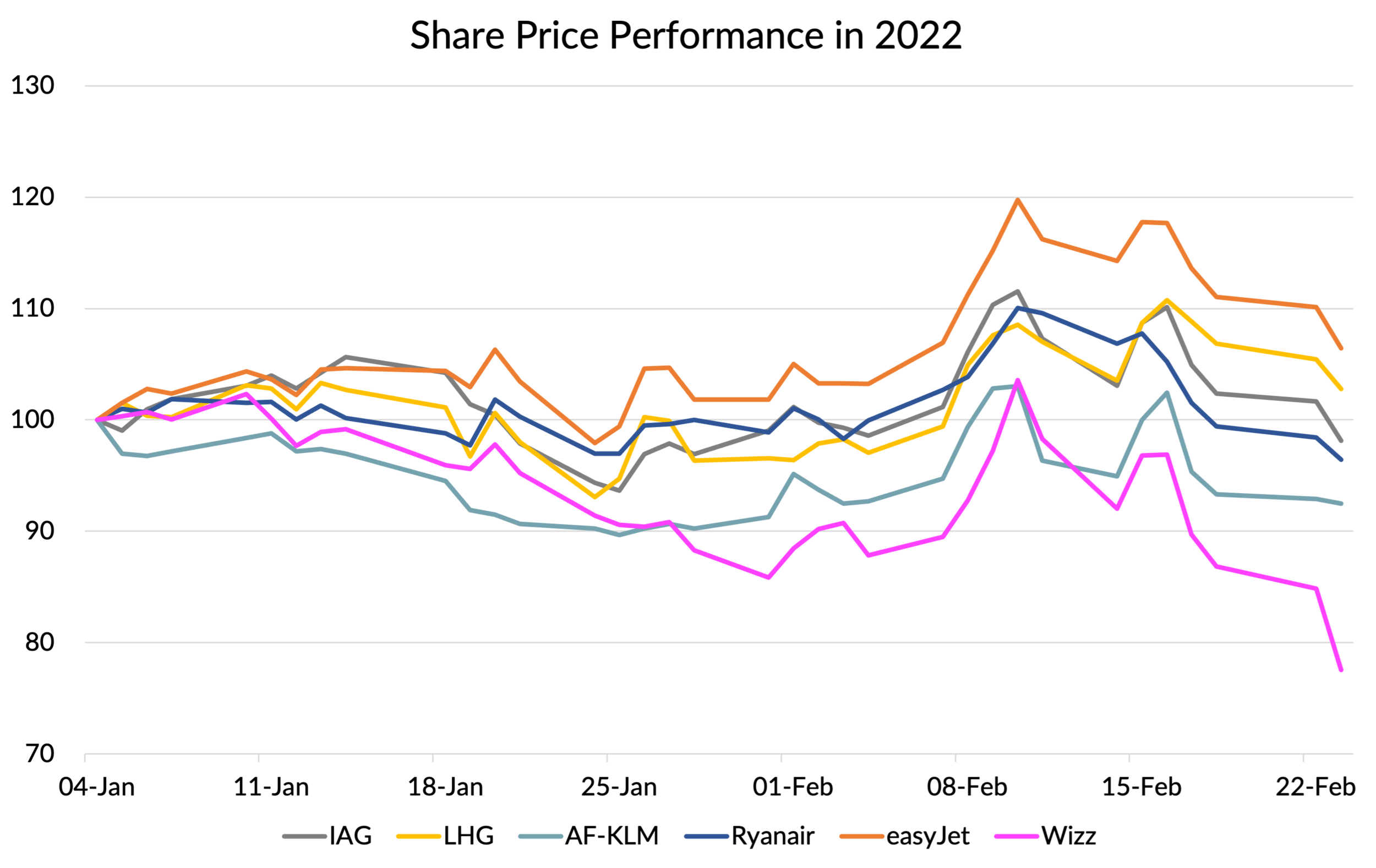

Despite broader problems in the world’s stock markets, airline share prices started the year relatively well. As I predicted, the Omicron wave was sharp, but also relatively short. With the impact on health care systems at the more benign end of the possible range of outcomes and governments relaxing most travel restrictions, a solid recovery in travel was setting in with many airlines and other travel companies reporting new bookings hitting or even exceeding pre-crisis levels.

The news from Ukraine has put an end to that positive stock market performance, with airline share prices slumping again in recent days.

Part of that impact is a general stock market effect. There will be an impact on economic growth and an increase in risk aversion from investors. Neither is good for equities and airlines are “high beta” stocks whose rises and falls will tend to be amplified versions of overall stock market movements.

However, there are also some very specific impacts of the crisis on airlines, especially in Europe. What are those impacts, and which airlines might be more or less impacted?

Direct capacity operated to Ukraine

The most obvious impact is on airlines with flights to Ukraine. The chart below shows the seat capacity operated within, to or from the country. I’ve colour coded the airlines by type. In red are the Ukrainian airlines, in green the Russian airlines. Western network carriers are coloured in blue and the low cost carriers in yellow.

In absolute terms, the most exposed is Ryanair, but of the Western airlines, WIzz Air is the most exposed relative to the size of the airline. About 8% of their seats in January were operated to or from Ukraine.

Source: OAG, Gridpoint Analysis

Demand impact

We know from the Gulf War that war can cause suppression of travel even in unaffected areas. US and Japanese tourists avoided Western Europe due to its “proximity” to Kuwait. Ukraine is in Europe and therefore likely to cause greater concerns about travelling to the region. Turkey and Eastern Europe seem likely to be particularly impacted.

There will be an overall impact on economic demand and confidence which will hit travel too. If the conflict escalates, things could be much worse of course.

Overflights

Another issue is the need to avoid overflying Ukrainian airspace, compounded by Belarus now being off limits. The most impacted airlines are those that are based nearby. For a carrier like British Airways which might normally overfly Ukraine en route to Singapore, diverting round the country only adds something like an extra 65 km to the flight distance. But it is more of a diversion for flights to Asia from airports like Vienna and Warsaw. Also impacted are North-South flights between Turkey / the Middle East and Scandinavia.

On the map below, I’ve shown the impacted routes from Vienna, Warsaw, Istanbul and Helsinki to illustrate the issue.

It will become a much bigger issue if overflying Russia became impossible, as it is a huge country which is very hard to avoid for routes from Europe to Asia. Russia is well aware of that fact and overflying charges are set at eye-watering levels as a consequence (contrary to international guidelines). It has threatened to block overflights before in retaliation for Western sanctions, so the risk is real.

Avoiding Russian airspace would add up to 20% extra distance for north Asia destinations and something like 10% for places like Hong Kong. As well as the additional time and cost involved, it would reduce the competitive advantage that European airlines have of offering direct flights from Asia to Europe, compared to transferring via Istanbul or the Gulf.

Finnair’s entire business model is built on acting as a transfer hub from Europe to Asia - avoiding Russian airspace is essentially impossible for them. A large amount of their business comes from the Russian market too. This could represent an existential threat to the airline in a worst case scenario.

But if Russia does restrict access to its airspace to Western airlines, non-NATO member Finland might escape and Finnair could even therefore be a beneficiary, along with Asian airlines and the Gulf carriers.

The impact on the fuel price

However, probably the biggest issue at the moment of events in Ukraine is what it is doing to the oil price. The media are focusing on the rise in the spot price of oil, which is now close to $100. Many airlines will be well hedged in the short term and will be watching the forward price more closely - those are the levels that they expect to pay in the future and also the prices that are relevant for new hedging contracts. The news there is slightly better, but still worrying. The price for Brent crude for July delivery is up from below $80 at the start of the year to about $94 today.

Will airlines be able to pass fuel cost increases in higher prices?

Economic theory tells us that an increase in input costs that affects all competitors will tend to be passed on in higher prices. In markets where demand is “elastic”, that increase in the general level of prices will dampen demand and supply will need to adjust downwards to bring supply and demand back into balance at the higher price level.

Despite having a customer base which is very price sensitive, and therefore likely to be very “elastic”, low-cost airlines take the view that there is a “trading down” effect which offsets this. For every passenger deterred from travelling by a price rise, they gain one who makes the decision to trade down from a more expensive airline. In fact, they will generally deny that they pass on a fuel price increase in higher fares at all, knowing that they need to maintain the low “headline fares” that are such a big part of their marketing and PR messaging. But in truth, they’ll be looking to find ways to offset their cost increases with additional “ancillary revenue”, which generally means higher fees for baggage or preallocated seating.

What this means in practice is that low cost carriers don’t tend to respond to higher fuel costs with reduced capacity - they expect the “legacy” carriers to bear the brunt of the capacity adjustment process and in the past the legacy carriers have obliged, pushing up fares and reducing capacity. Will that happen this time round?

Maybe. But one thing that I would say is that in “normal” market conditions, network carriers have long-haul and the relatively less elastic business traveller demand to fall back on. They can afford to lose a bit of market share in price sensitive short-haul market segments. That will be much less the case in current market conditions. Network carriers have only just pulled the trigger on bringing back capacity as COVID restrictions have eased - they will be very reluctant to start pulling back again.

The other factor is that the market share of low-cost carriers is now much higher. The “trade-down” effect is therefore weaker and low-cost carriers are increasingly fighting each other for share. What this means I think is that if fuel prices do continue to go up, it is going to put pressure on the weaker low-cost players.

There is an important factor that plays into this, of course. The impact of fuel hedging policies. Let’s look at that next.

Hedging

Of the major European carriers, Ryanair is the most highly hedged. They just gave figures of 100% hedging for Q1, 80% in Q2/Q3 and 70% in Q4/Q1-23, so over 80% for the full calendar 2022 year.

Air France - KLM also gave a recent update and are 72% hedged in Q1, 63% in Q2, 42% in Q3 and 28% in Q4, so just over 50% for the year as a whole.

EasyJet say they are 60% hedged for the first nine months of 2022, which is very similar to AF-KLM for the same period.

We’ll find out where Lufthansa Group and IAG are when they deliver their Q4 results in the next few days, but based on figures they provided three months ago, I expect them to be at least as well hedged as AF-KLM and probably a little higher.

In Europe, the outlier is Wizz, who I understand to be essentially unhedged.

Ryanair versus Wizz

It is no surprise to me that Ryanair is the most highly hedged. They understand the value of being perceived as the strongest player when high fuel prices put pressure on airlines to cut capacity. They can afford to give up some margin in a low fuel price environment to allow them to put pressure on competitors when times get tough.

For whatever reason, Wizz have taken a completely different approach. Combined with their relatively high direct exposure to Ukraine and adjacent regions, a highly price sensitive customer base and a strategy which is focused on ultra high growth, they seem quite vulnerable to me.

CEO Józef Váradi has been talking about his intention to build the company into a 500 aircraft operation - bigger than Ryanair is today. That will be perceived by Ryanair as a direct challenge and is likely to see an aggressive response. I think that the heavily hedged Ryanair is very likely to use the financial firepower that gives them to take its smaller rival down a peg or two, perhaps by transferring capacity from Ukraine into directly attacking some of Wizz’s strongholds in other parts of Eastern Europe.

Wizz versus easyJet

WIzz will hope that Ryanair points its guns elsewhere and that WIzz’s own cost advantages compared to everyone except Ryanair will enable it to continue its supercharged growth, even in a high fuel price environment.

Its move into Gatwick is of particular significance I think, as it can be seen as a direct attack on easyJet. Whether it is done by organic share gains or by merger or acquisition, I think that’s a battle it needs to win if it is to have any chance of achieving its goal of matching or overtaking Ryanair in size in Europe.

Final thoughts

As was the case with COVID, the significance of today’s news from Ukraine goes far beyond its impact on the airline industry. I don’t want anyone to think that by focusing on that I am in any way playing down those wider issues. For me, writing about this is in part a coping mechanism. There is so much of what is going on that I cannot pretend to understand fully and can certainly do nothing about. My heart goes out to the people of Ukraine and to anyone else who might get dragged into the horror of war.

The challenges faced by airlines are minor in comparison, but they still represent another kick in teeth for an industry still struggling to emerge from the near death experience of the pandemic.

Let’s hope for everybody’s sake that the we’ll get some better news in the days and weeks ahead.