Waiting for a vaccine: the big three European network airlines in Q3

Q3 results for Air France - KLM, Lufthansa and IAG

All three of the big European network airline groups have now published their September quarter results. They made pretty ugly reading as the nascent recovery in European travel was snuffed out by a resurgence of the virus.

However, there were some interesting differences to be found in how each company is managing the crisis and trying to get themselves into shape to benefit from the recovery, when it comes.

Comparing the numbers

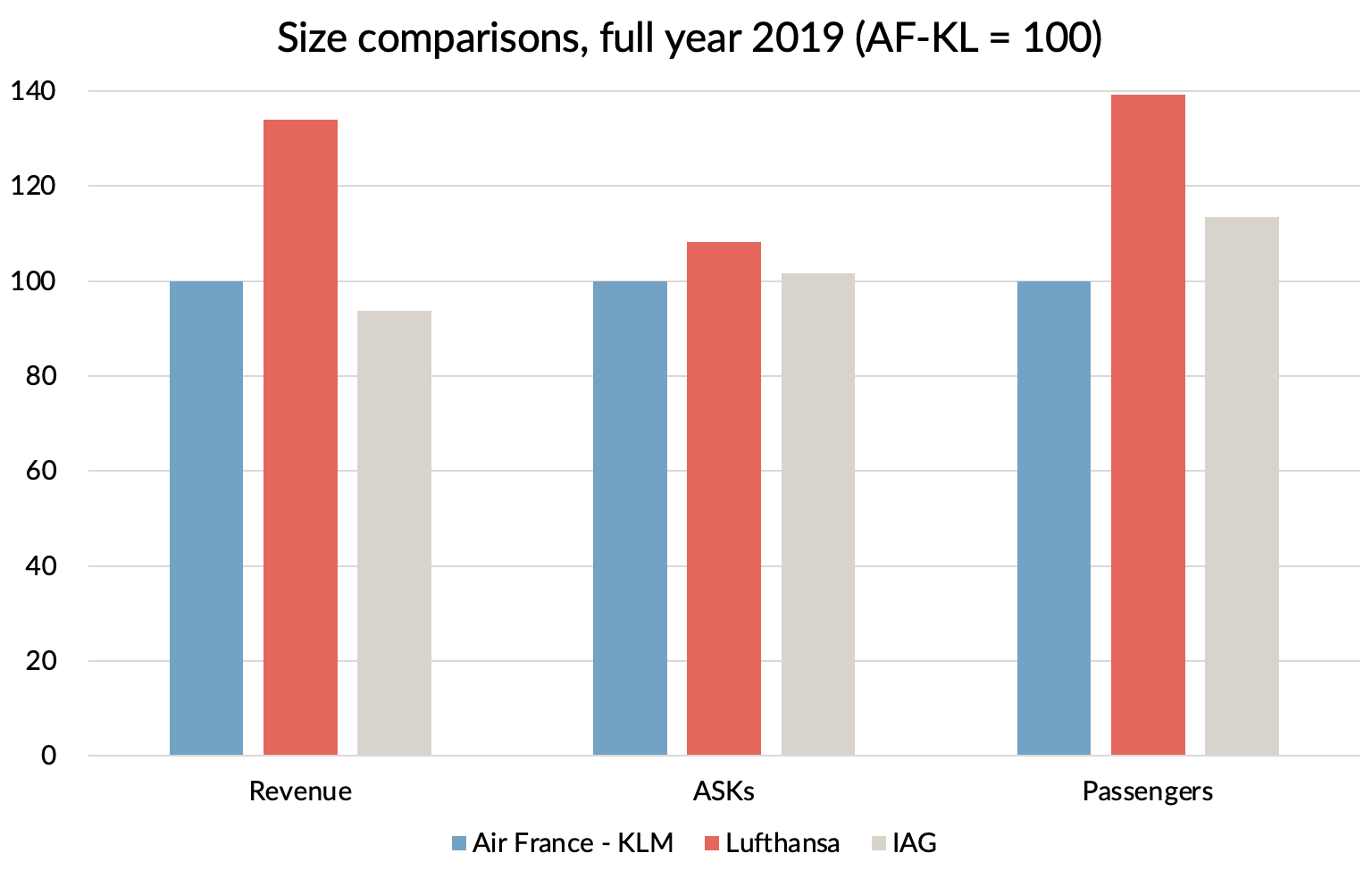

Before I start comparing the numbers, I need to explain why I am going to use absolute numbers to do many of the comparisons, rather than ratios which would be more normal. The reason is that most of the denominators that I would normally use, like revenue or ASKs are pretty meaningless at the moment. Fortunately, the three groups were pretty similar in size before the crisis.

Source: company reports

In 2019, IAG and AF-KL reported almost identical total revenues and passenger capacity was quite similar too.

It is true that Lufthansa was a 33% bigger company when measured by revenue, in part because it had big non airline businesses such as its catering business, LSG. However, its passenger airline business was about the same size as the other two when measured in ASKs.

Operating losses

The headline operating losses before exceptional items for Q3 were pretty similar, with the prize for losing the least going to AF-KL. The company managed to lose just over a €1 billion in the quarter, compared to €1.3 billion at Lufthansa and IAG.

Q3 2020 operating loss, before exceptional items. Source: company reports.

In trying to explain what lay behind this differential performance, I will start by looking at capacity and revenue.

Revenue performance

Passenger revenue had already been hit in Q1. That mainly impacted Asian routes, which hit Lufthansa hardest as it has the highest exposure to that region.

Revenue was virtually non-existent in Q2, with all three groups coming close to a full grounding of their operations.

In Q3, all three groups began to bring back capacity, with AF-KL bringing back more. That translated into better revenue performance too. As a percentage of 2019 levels, AF-KL made almost double the passenger revenue in the quarter as IAG did.

Source: company reports

Passenger revenue performance was very different between short-haul and long-haul, so I’ve looked at the figures for each separately.

In short-haul, AF-KL flew the most of the three and managed to translate that into stronger passenger numbers, with load factors quite similar between the carriers.

Long-haul was much more depressed during the quarter, with many markets still subject to travel restrictions. Note the different scale on the following chart.

The performance difference here was even bigger. IAG was the worst, with long-haul RPKs only 6% of last year’s levels.

AF-KL added back more than twice as much long-haul capacity as the other two, and managed to achieve similar load factors. That was helped by relatively strong performance to the French overseas territories. These are long-haul domestic markets, which didn’t have travel restrictions. AF-KL performance in other long-haul markets wasn’t much different to Lufthansa’s and IAG’s.

In normal times, 35% would not be a cash positive load factor. However, the inflated cargo yields at the moment are making flights cash positive even without any passengers at all in some cases.

Let us have a look at how each company did in cargo.

Cargo revenue

Compared to the others, AF-KL were a little slow in taking advantage of the cargo revenue opportunity caused by the shortage of passenger belly capacity in Q2. But they made up for lost time in Q3 and were the strongest performer of the three, perhaps at the expense of Lufthansa, where cargo revenue registered a small decline on 2019 after strong growth in Q2.

Although IAG has been doing quite well versus last year, its cargo business is by far the smallest of the three, with revenues in the third quarter of €300m around half the levels achieved at the other two carriers. That’s driven by a mixture of geography (the UK is not much of an export economy) and past strategic decisions not to operate a dedicated freighter fleet.

Cost performance

With revenue heavily down, the scale of operating losses was largely dictated by the ability to slash costs. The biggest challenge with such a big drop in activity was cutting fixed costs, especially employee expenses.

IAG cut employee costs by 42% in the quarter, slightly more than the other two which reduced by 36%. Both IAG and Lufthansa attributed about half of these reductions to government schemes such as short term working and salary support programmes. Rather more of AF-KL’s savings came from that, with support in the quarter amounting to 72% of their savings.

Source: company reports, GridPoint analysis

Looking at costs more broadly, it is quite striking how much lower employee costs are at IAG in absolute terms, reflecting both its bigger cuts and its lower starting position. Other cost categories are more similar, although IAG tends to have the advantage there too.

In the above chart, I adjusted Lufthansa’s numbers to exclude their catering business, which is labour intensive and tends to distort the comparisons. Before the crisis hit, Lufthansa was working hard on selling off that non-core business. Perhaps for an apples to apples comparison, I also ought to exclude the MRO and cargo businesses. But although these are larger at Lufthansa than at IAG and AF-KL, all three airlines have those activities and to exclude them would require me to make too many assumptions.

Employee numbers

Lufthansa has said that it needs to find employee cost savings equivalent to cutting about 27,000 employees, about 20% of its total going into the crisis. Management made a big thing about having already achieved a 14,000 drop in group employee numbers compared to December 2019. But 10,000 of those were in the catering division, which saw a 29% reduction. These job losses are almost certainly outside Germany and in less unionised environments.

Employee numbers in the core airline fell by only 4,000, or about 3%. Lufthansa is reducing management headcount by 20%, but that won’t take effect until Q1 next year. Agreement has been reached with cabin crew to reduce costs, mainly through crew working reduced hours, but the company has agreed not to make any compulsory redundancies. No long term agreement has yet been reached with pilots or with ground staff. Management warned that it may take them until the middle of next year before they can force headcount reductions in Germany, if no union agreement is reached.

The following chart shows the trend of employee numbers over time, with the catering division excluded from the Lufthansa numbers.

At AF-KL, employee numbers have dropped by 5,400, over half of that from releasing temporary employees. They have reached agreements with their unions to shed 9,000 FTEs by the end of 2020 and a further 5,500 by 2022. That’s about 15% of group employees and seems strangely unambitious in both size and speed given the scale of the crisis.

IAG have been moving much faster on cutting jobs, especially in the UK where the government’s COVID furlough scheme was due to expire at the end of October. It reached agreement with unions at British Airways for cuts of about 10,000 staff, about a 25% reduction, and has been moving ahead with implementing these. At a group level, employee numbers have already dropping by 8,500 since last year, a 13% reduction. The UK furlough scheme has now been extended to the end of March 2021, which will be helpful over the winter period. With BA operating less than 30% of its normal schedule, it will still have many surplus staff despite the redundancies.

Capacity plans

IAG are planning to operate “no more than 30%” of normal capacity in Q4 and Lufthansa “below 25%”.

KLM plan to operate 45% of capacity and Air France below 35%, in both cases quite a bit more than at the other two airline groups.

So who did best?

AF-KL won the prize for the lowest losses in the quarter, operating more capacity and driving more revenue. They seem intent on trying to repeat the trick in Q4 and they may succeed. However, it will be more difficult to pull it off in the winter season with the second wave hitting its home markets.

IAG went into the crisis with lower costs and seems to be making faster progress on lowering them further. So far, it has struggled the most to find passenger demand and that is unlikely to change any time soon, with the UK going back into a one month lock-down in which non-essential travel is banned. But its lower costs will help it limit losses in the short term and should stand it in good stead once demand starts to return.

In the third quarter, Lufthansa’s performance was “in the middle” on most measures, combining AF-KL’s slower progress on cost reduction with IAG’s passenger revenue weakness. However, it is less of a pure-play passenger airline business than the other two and a bit of good old-fashioned diversification is helping it out at the moment.

However, the truth is that all three of these airlines are losing over a €1 billion a quarter and will continue to do so until demand climbs back off the floor. How long that will be, nobody really knows as it depends on the world getting on top of the pandemic.

Fortunately, the prospects for that are finally beginning to look better.

Good news on the prospects of a vaccine

Stock markets and airline shares took off today when Pfizer and BioNTech announced the results of their late stage vaccine trial, with effectiveness found to be over 90%. The combined market capitalisation of these three companies increased by €3.6 billion on the back of the announcement, with IAG shares in particular jumping by 38%.

It is perhaps no coincidence that this is exactly the amount these companies lost in Q3.

I guess the market has concluded that the recovery will come three months sooner than they believed yesterday.

Maybe 2020 is finally beginning to look up.