Ryanair posts a profit for the September quarter

Ryanair becomes the first airline in Europe to report a profitable quarter since the crisis began

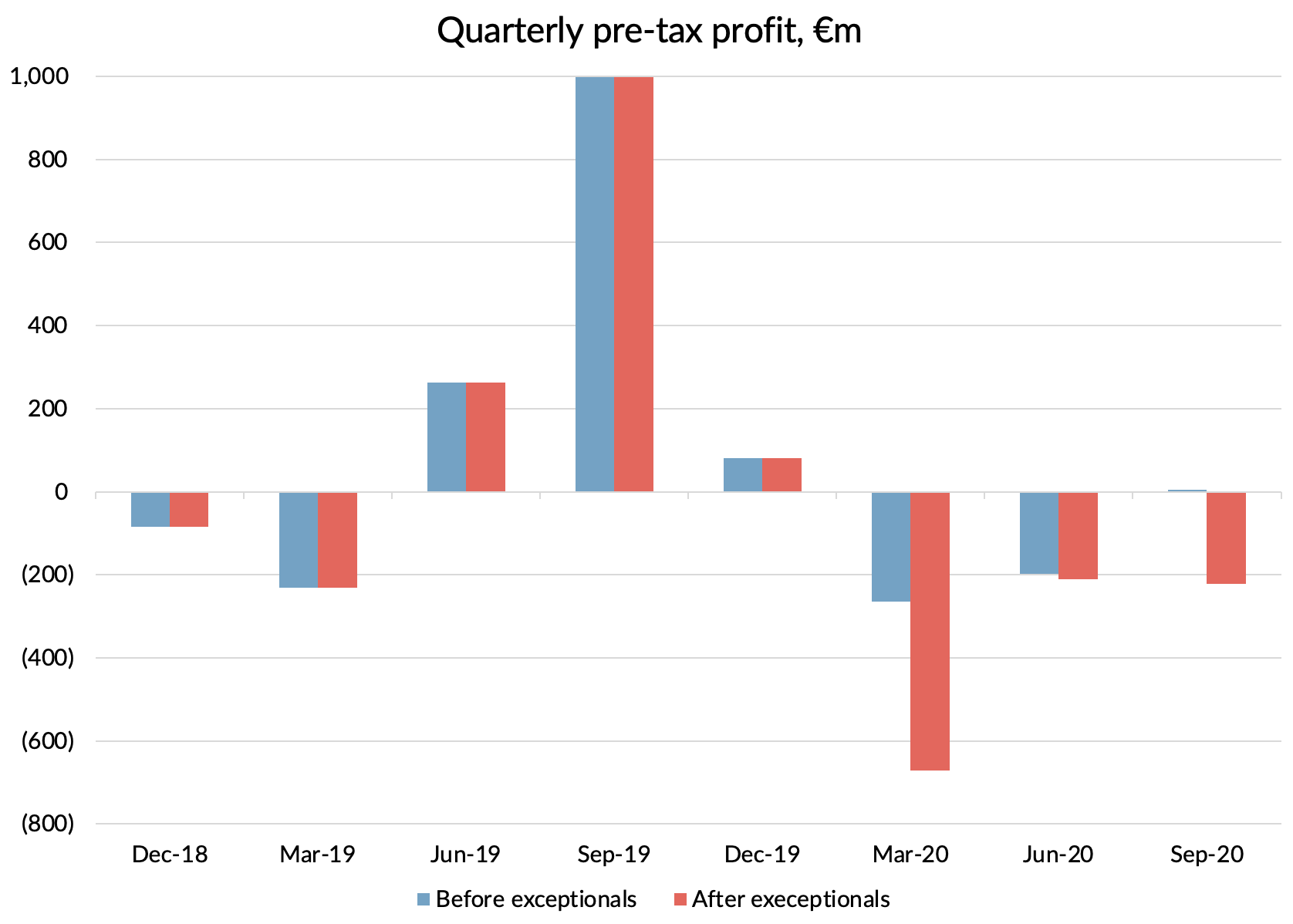

The headline result that the company focused on was the loss after tax figure of €197m for the first half. The pre-tax figure was almost the same at €192m. Both of those excluded an exceptional charge of €240m for ineffective fuel hedges, taking the total pre-tax loss for the first half to €432m.

Of more interest, I think, was the result for the September quarter in isolation. Before exceptional hedging costs, Ryanair actually managed to record a small operating profit of €10.8m and was still profitable after financing costs, delivering €4.9m pre-tax.

That is pretty impressive.

Granted, Ryanair made €1 billion of profits in the same quarter last year, but measured on the same basis, easyJet managed to rack up £315m (c.€350m) of losses for the same period.

Capacity and revenue

The company operated capacity at about 50% of 2019 levels for the quarter. Load factors of 72% were well down on last year and so passenger numbers were only 38% of last year. Revenue per passenger of €63 was down too, but only by 10%. That is surprisingly good in the circumstances, I think.

Overall, that led to revenue of €1.1 billion, down 73% on last year. The fact that Ryanair managed to make a profit despite this is testament to how low its costs are and also how variable they are with volume.

Operating costs

Some of the most impressive statistics from Ryanair's September quarter figures were the figures for unit costs. Despite the massive drop in volume, cost per seat was actually flat compared to last year. Excluding depreciation, cash cost per seat fell 7%.

Most of the reduction in non-fuel unit costs was driven by lower fuel cost per seat, which was down 17% versus last year. Given that the company was over-hedged during the period, this can't be down to the post COVID drop in oil prices. But Ryanair had probably hedged summer 2020 fuel at lower prices than the previous year. There should be a lot more savings to come from 2021 as hedges placed before the pandemic unwind.

The second biggest cost category, "Airport and handling costs" also fell faster than capacity, with unit costs down 10%. In the notes to the accounts, management made reference to having benefited from "reduced charges". There probably is an element of that in the numbers, with airports desperate for volume and Ryanair almost certainly driving a hard bargain, but it seems more likely to me that some of the costs in this category are levied on a per passenger basis and lower load factors therefore help reduce cost per seat.

The main area where unit costs has gone up is staff costs. The company did benefit from government grants, with €44m received in the first half, offsetting 16% of gross employee costs. However, that is a lot lower proportion than has been received by many others, for example Air France - KLM got 37% of their cost covered. Net of government grants, staff cost per seat went up by 16% in the quarter. However staff costs represents a much lower proportion of the cost base for Ryanair than at most airlines (only 15% in normal times), so this had less of an impact than it might have done.

Cash and balance sheet

Net debt went up by only €210m in the quarter, helped by a €400m equity issue. Adjusting for that, operations therefore burnt about €610m of cash.

A lot of that was accounted for by the company finally catching up on its customer refunds, with €1.5 billion of customer refunds now having been paid out or turned into vouchers. They obviously took in new bookings too, so I think there was a net cash outflow of about €800m in the quarter relating to this.

Helping to offset that was an interesting negative figure for capital expenditure in the quarter of €280m. It seems to me that that can only relate to refunds of pre delivery payments from Boeing. The first downpayment perhaps by Boeing on the final settlement for 737-MAX delay compensation.

With net debt of only €1.1 billion and 80% of their aircraft owned debt free, the company is extremely well placed to withstand what will be a very difficult winter for the industry.

Outlook

Like other airlines, Ryanair declined to give any guidance for profits. They did say that they were planning on operating about 40% of 2019 capacity during the winter season, with a likelihood that this may go down further in response to the recent increase in European lockdowns. For summer 2021, they said they had scenarios ranging from 50% to 80% of 2019 levels. Where they end up will depend on developments in the pandemic and government responses to it. I think that the 80% case is probably linked to an assumption of a vaccine being widely deployed in Q1 or Q2 next year, which was mentioned as a possibility by Michael O'Leary.

Final comments

Overall, an impressive set of results in the circumstances. I suspect Ryanair will be the only airline in Europe that manages to report a profit for the quarter, although perhaps Wizz will manage it too when they report on Thursday. The rest of the year will clearly be loss-making, since it is during a normal year and market conditions have worsened too. But Ryanair has demonstrated its ability to weather the storm better than others.

The 737-MAX deliveries will finally start rolling in next year and Ryanair will undoubtedly have secured rock bottom prices. The aircraft come with a 14% advantage in fuel burn compared to previous generation aircraft.

Other airlines had better redouble their efforts on cost through the winter and bolster their balance sheets.

Micheal O'Leary is coming for you.