Record losses for 2020 at IAG

IAG reports 2020 loss of £7.8 billion

IAG racked up another €1.6 billion of pre-tax losses in the final quarter of 2020 to bring the total loss for the year to an eye-watering €7.8 billion.

€3.1 billion of the full year losses were marked as exceptional, with losses on fuel hedging alone accounting for €1.7 billion. There were almost €1 billion of fleet and other asset write-downs and €0.3 billion of employee restructuring costs to pay for 10,500 redundancies, mainly at British Airways.

Excluding these exceptional charges, pre-tax losses of €1.3 billion for the quarter were slightly better than Q3, but the €2.7 billion raised in an emergency rights issue in September didn’t even cover the €3.1 billion of after tax losses in the second half of the year.

Source: Company reports

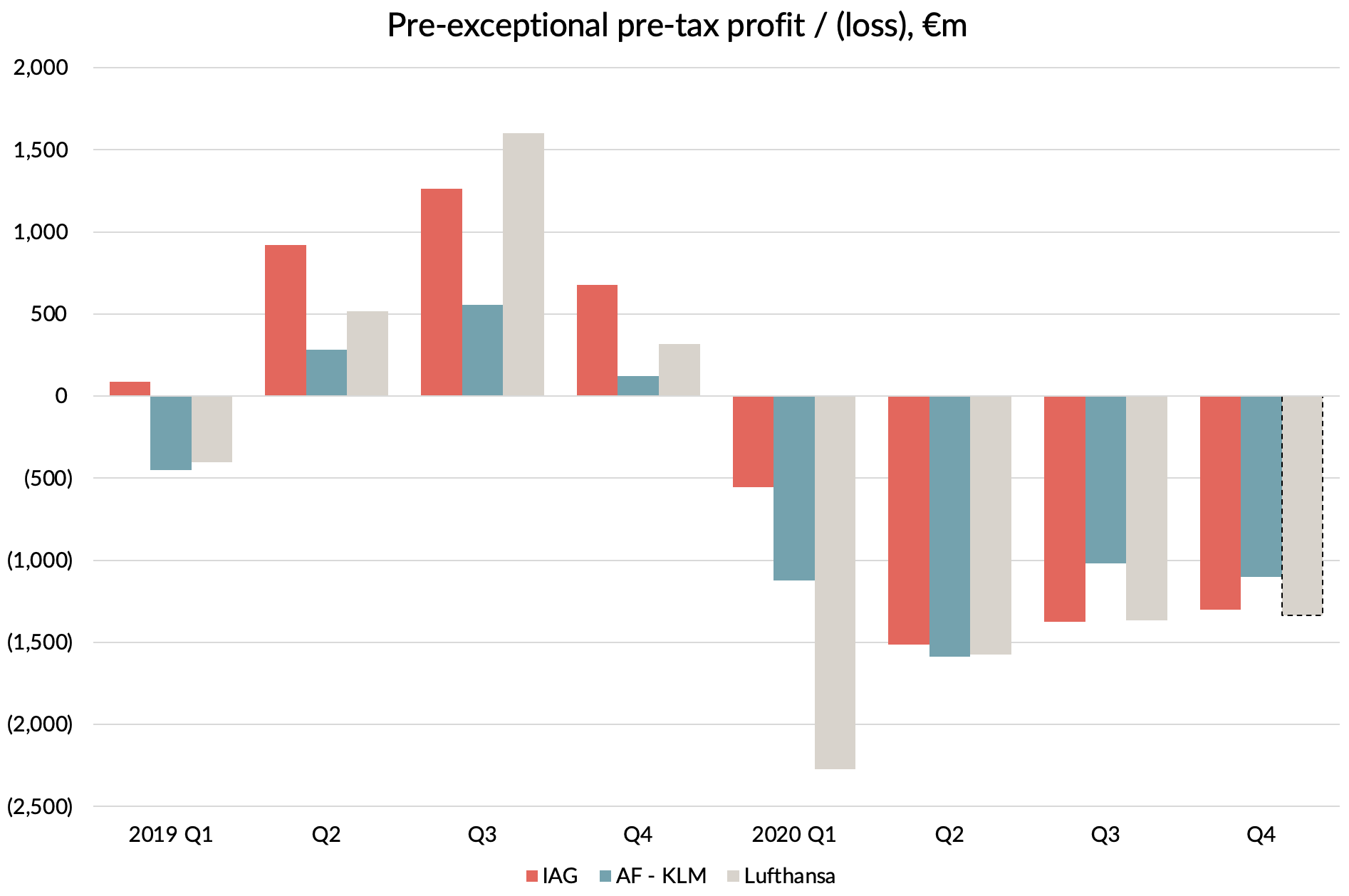

Comparison with Air France - KLM and Lufthansa

Although IAG performed much better than AF-KLM in 2019 and in the first half of 2020, the situation was reversed in the second half and AF-KLM ended the year with pre-tax losses of “only” €6.9 billion.

We haven’t had Lufthansa’s Q4 results yet, but based on analyst consensus forecasts, they will probably win the prize for the biggest 2020 losses amongst the European airlines, with pre-tax losses topping €8 billion.

Before exceptional items, Lufthansa and IAG seem to be performing very similarly in the second half, with Air France - KLM doing a bit better.

Source: Company reports. Q4 2020 for Lufthansa is estimated based on analyst consensus.

Why is Air France - KLM doing better?

AF-KLM’s pre-tax losses before exceptional items were €559m lower than IAG’s in the second half. That was more than explained by the €2.3 billion of additional revenues that they generated, which were almost double IAG’s. Part of the story was that AF-KLM has a dedicated freighter fleet and their central location in Europe helps cargo too. But passenger revenues were also much better, driven by resilient markets to French overseas territories and KLM’s effective strategy of concentrating short-haul flows over its Schiphol hub.

Source: Company reports

Whilst we don’t yet have Lufthansa’s Q4 numbers, it is clear that their results will also have been delivered with much higher revenues. Q3 revenue was €2.7 billion, slightly more than IAG managed in Q3 and Q4 combined.

IAG’s cost performance

IAG did much better than AF-KLM on the cost front. Its unit costs were about 20% lower to start with as I outlined in this earlier post. The biggest gap before the crisis was in employment costs, where IAG was 45% lower, driven by a roughly equal mix of average pay and productivity.

Both carrier groups reduced employment costs in the second half compared to 2019. IAG’s 45% reduction was slightly better than AF-KLM’s 43%, but that is perhaps not surprising given the additional capacity operated by AF-KLM. The main difference was the make-up of the cost reduction, with far more of AF-KLM’s coming from temporary government wage support programmes. For the year as a whole, AF-KLM got over €2 billion of such support, compared to €0.7 billion at IAG.

Source: Company reports

Much more of the adjustment at IAG was made through job reductions, with 14,350 fewer people employed at the end of 2020 compared to a year earlier, a reduction of 20%. The equivalent figures at AF-KLM were 7,064 and 8%.

Source: Company reports

A closer look at Vueling

Whilst the comparisons with other network airline groups show IAG delivering superior cost performance to offset revenue shortfalls, I also thought it would be interesting to look specifically at Vueling, IAG’s low-cost carrier, to see how it performed relative to AF-KLM Group’s Transavia and to the big two low-cost specialists in Europe.

In terms of capacity operated compared to 2019, Vueling was “in the middle”. However, it performed worse than any of the other three carriers in terms of costs (which fell less) and also revenue (which fell more), as shown in the chart below.

The main issue on the revenue side for Vueling was the load factor. At 59% this was some way below Ryanair’s 71% and easyJet’s 74% for the same period. Although Transavia’s load factor of 64% was also worse than the big two, it was still better than Vueling’s, despite operating the most capacity of all these carriers compared to 2019.

On the cost side, it is hard to tell why Vueling’s performance was so poor. IAG don’t provide much of a breakdown of the cost figures. We do know that for the full calendar year, employee costs fell only 35% compared to a 44% fall at Ryanair for the same period, despite the bigger shrinkage in capacity. So it looks like some of the gap was there.

At Ryanair, depreciation fell by 23% due to the way it varies its depreciation charge based in part on usage, whilst both easyJet and Vueling charge fixed amounts per month. In fact, Vueling’s depreciation charge went up in 2020 versus 2019 as it took delivery of new generation A320 NEO aircraft.

Whatever the reasons, Vueling managed to accumulate an operating loss for the year of €623m before exceptional charges, only slightly less than Ryanair’s €761m, despite Ryanair being 3.5 times Vueling’s size.

In terms of operating margin, Vueling was the worst performing part of IAG in 2020. For an airline with a business model that is supposed to be more resilient in a downturn, that is somewhat embarrassing.

Looking forward for IAG in 2021

Guidance for cash costs for the first quarter of 2021 was for a reduction of €30m/week compared to the fourth quarter, so that represents a €385m cost saving.

But revenues will also be down, with lockdowns, flight bans and draconian travel restrictions in the UK in place until at least 12th April and cases still high across Europe. The company guided that Q1 capacity levels would be around 20% of 2019, compared to the 27% operated in the final quarter of 2020. If passenger revenues fall proportionately to capacity, even if cargo and other revenues perform in line with Q4, that would be a revenue reduction of about €210m.

So there is a chance that losses may narrow in Q1, but it still looks to me like 2021 will start off with another €1 billion or more of quarterly losses.

There is hope for much better figures from the second quarter onwards. Like other UK airlines, British Airways saw a big jump in bookings following the UK Prime Minister’s “end to lockdown” plan announced on the 22nd February.

Source: IAG results presentation

The stock market is certainly beginning to anticipate a vaccine-led recovery kicking in from the second quarter and IAG shares are up 24% since the start of the year.

Let us hope that this isn’t another false dawn, as there are only so many €1 billion plus quarterly losses than any company can withstand.