Here we go again

The UK’s red list is back

It was nice while it lasted.

For 25 days, there were no countries on the UK’s travel red list. But with the recent discovery of a potentially worrying new variant (B.1.1.529, dubbed “Omicron”), six southern African countries have been put back on the list (Botswana, Eswatini, Lesotho, Namibia, South Africa and Zimbabwe). The US, Canada and the EU have also imposed flight bans on the same countries, with most adding Mozambique and some also Malawi.

Update: Even as I was posting this, the UK government announced they were adding both of those countries and also Angola and Zambia to the red list. They also said all arriving passengers would need to take a PCR test and self-isolate until they were confirmed as negative.

From a travel volume perspective, the most significant of these countries is South Africa. It’s a market for which Christmas is peak season, and after many months languishing on the UK’s red list, there was also lots of pent up demand for families desperate to reconnect. It was removed from the red list only seven weeks ago, and had been shaping up to be one of the bright spots for British Airways and Virgin Atlantic this winter.

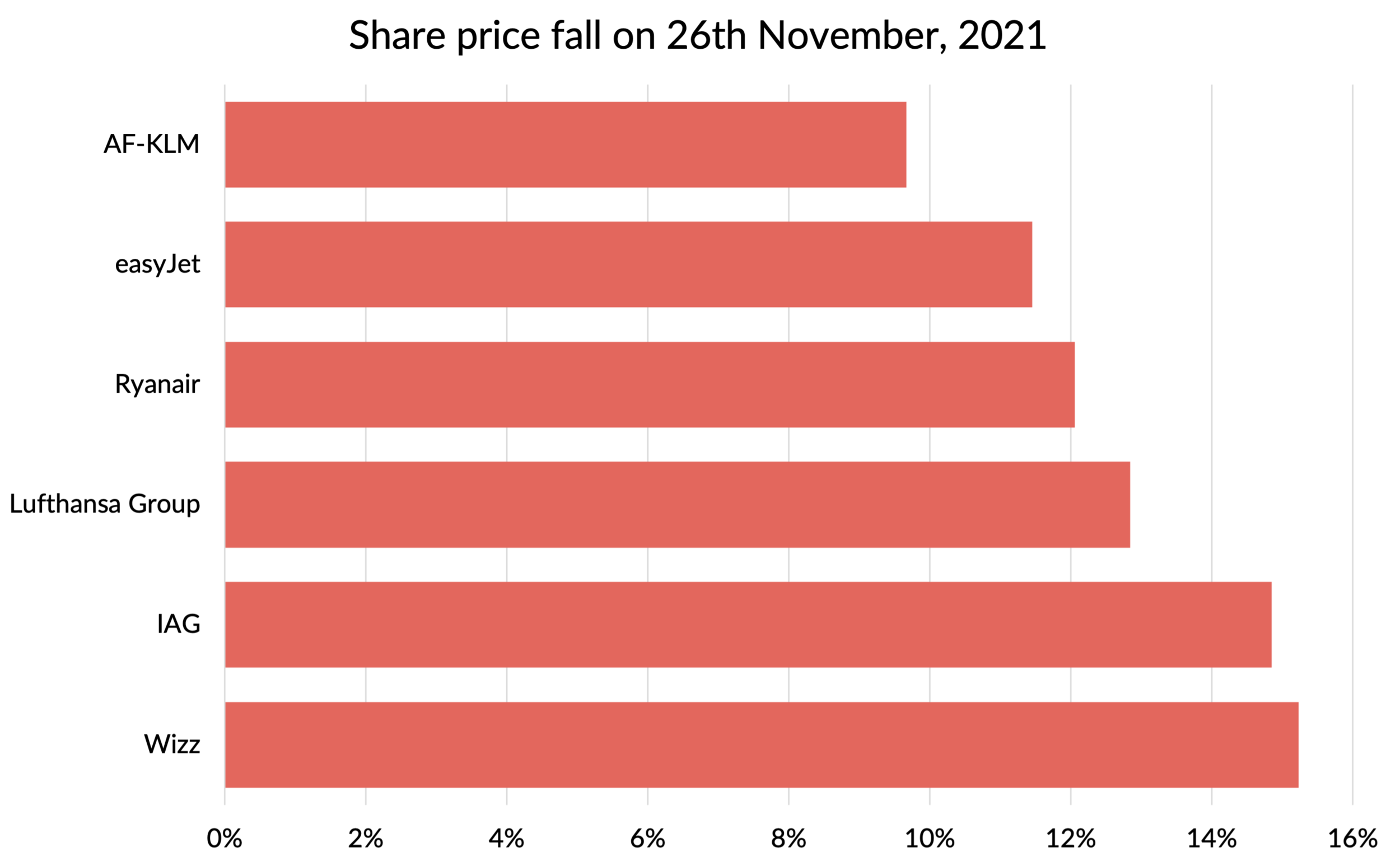

Impact on airline shares

Investors feared the worst, with airline shares falling across the board by double digit percentages. There wasn’t much to choose between the big European airline stocks, with network carriers and low cost carriers all being hit.

It isn’t the specific impact of flight bans to a few African countries that is hitting airline shares, it’s the fear that Omicron could be significantly worse than Delta, and as it spreads across the world it will give rise to a reimposition of travel restrictions across a much wider geographic scope.

Source: Yahoo Finance, GridPoint analysis

How worrying is Omicron?

The truth is that we don’t yet know how worried we should be about this new variant. For those who want to read a good account of what we do know, I can recommend this twitter thread by FT journalist John Burn-Murdoch. In summary, Omicron has a number of mutations in parts of the virus that are known to be important for its ability to spread. But so did many other variants that proved not to be a big deal. But what has got people concerned is that it’s been growing fast in South Africa, at a time when Delta cases had fallen to low levels, so it looks like it is able to outcompete Delta. New waves of infection can happen without being linked to new variants, so it could just be a coincidence. We’ll know more over the next few days, but in the meantime policy makers are assuming the worst on a precautionary basis.

Experts acknowledge that if it does turn out to be significantly worse than Delta, travel restrictions will only slow down its spread. A few cases have already been detected in Belgium, Germany and the UK, so the chances are that it is already spreading in the community in many places across the world.

However, with much of Europe already struggling to cope with a big growth in cases, making the situation worse this winter with an even faster spreading variant is the last thing policy makers want. Even if the best that can be done is to slow down the spread, that’s likely to be pursued to buy time to complete booster programmes and “flatten the curve” to allow healthcare systems to cope. We all know the drill by now.

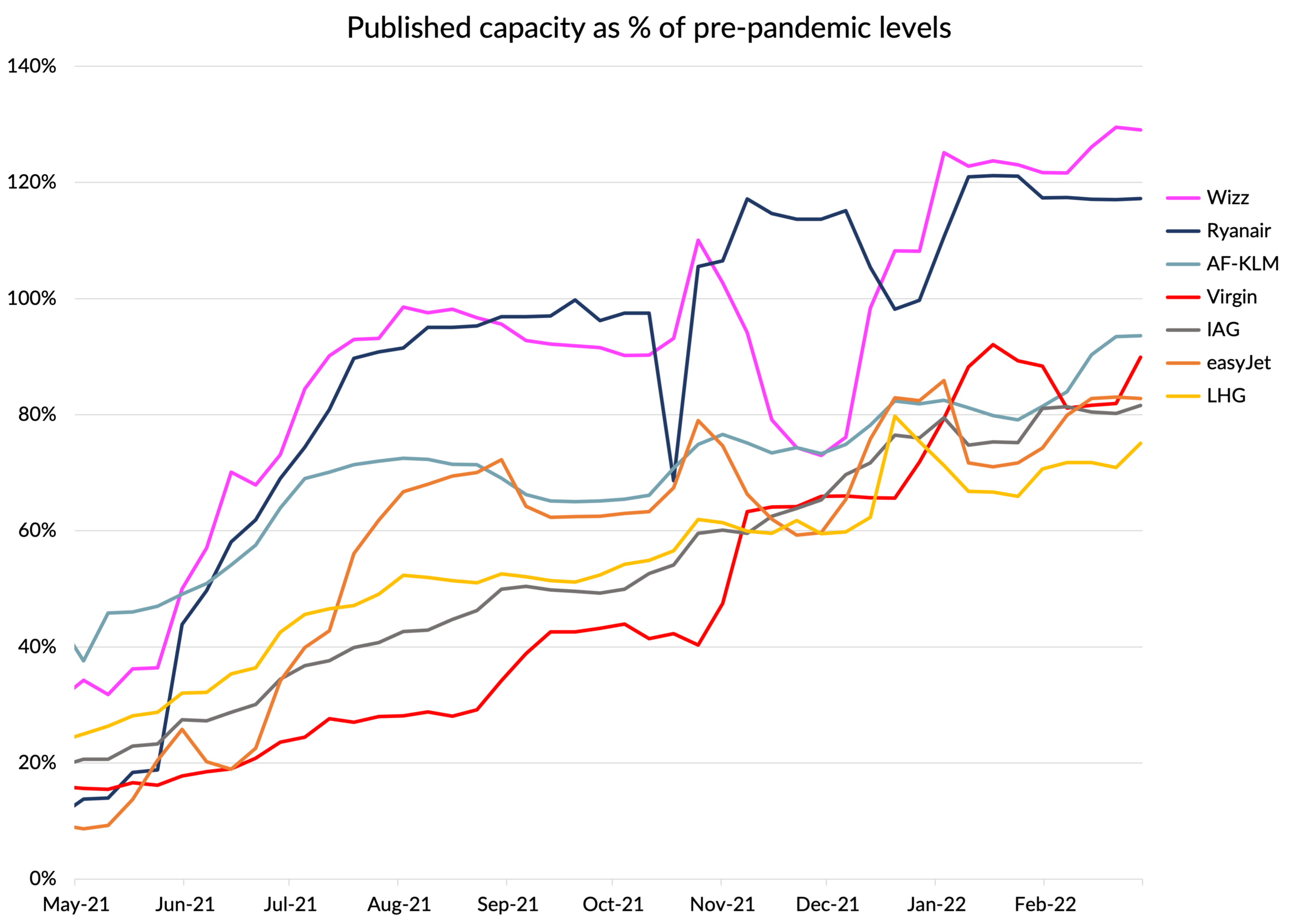

What does this mean for airline planners?

Most airlines in Europe have been gearing up to get back to something like pre-pandemic capacity in 2022, as bookings have surged following the general relaxation of travel restrictions in recent weeks.

The next chart shows how the weekly published capacity has developed during 2021 and how it currently looks for the rest of the winter season. I’ve expressed it as a % of 2019 and shown the figures for the big three network groups and the big three low-cost airlines in Europe. I’ve included long-haul specialist Virgin Atlantic as another interesting reference point.

You can see that Wizz and Ryanair are planning capacity at around 120% of 2019 levels by the end of the winter season. The others are all bunched around the 80-90% level.

Source: OAG, GridPoint Analysis

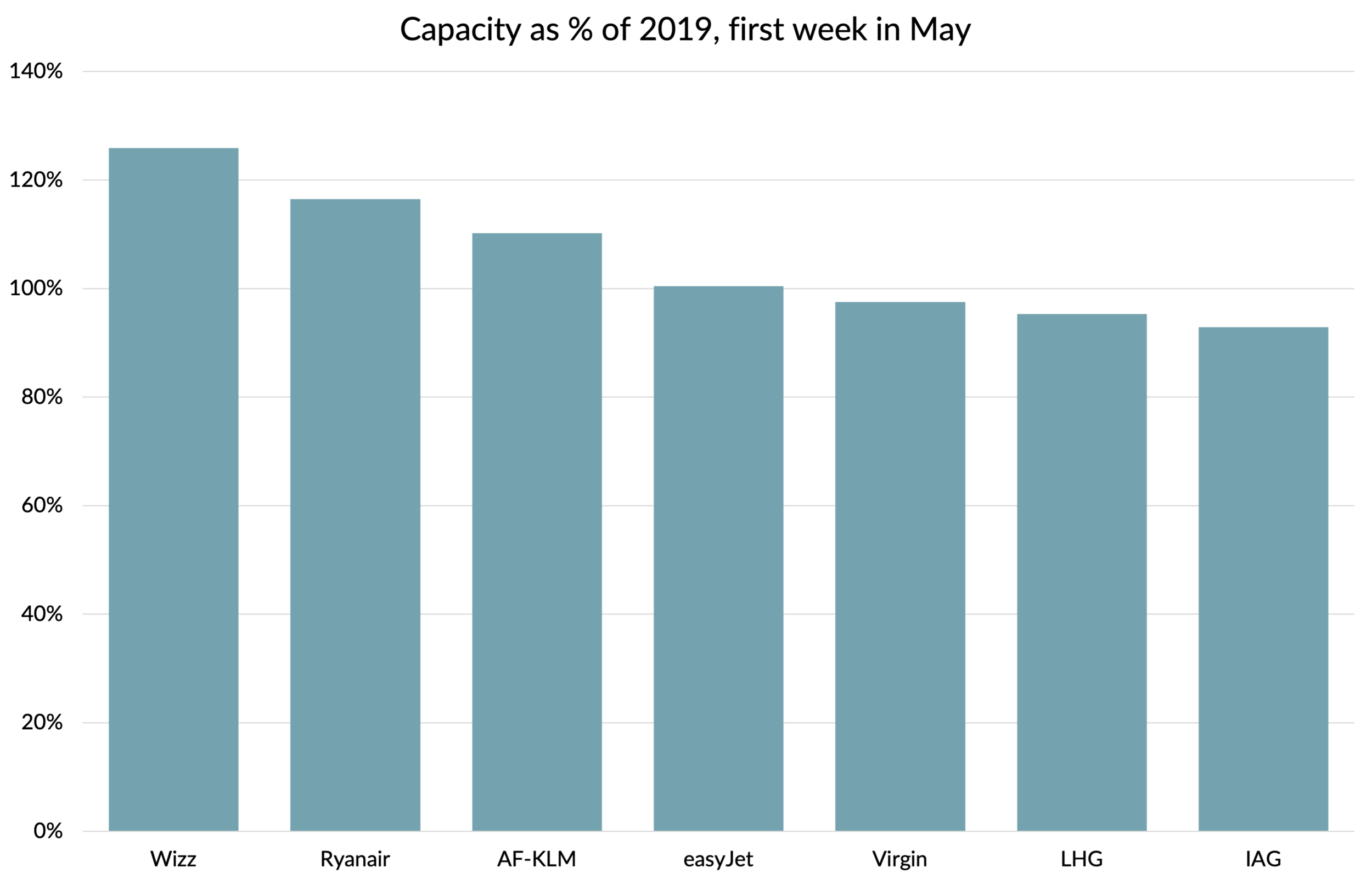

Published plans for Summer 2022 are still perhaps a little unreliable, but the figures for May 2022 show capacity above or close to 2019 levels across the board.

With Summer 2022 plans being finalised in the run up to the IATA slot hand-back deadline in mid January, are airline planners going to have to go back to the drawing board over the Christmas holidays?

They will certainly hope not.

But with costs starting to be locked in as airlines get their planes ready to fly again and hiring plans proceed at pace, they’ll be anxiously watching for signs of whether Omicron will trigger a major shift back to travel restrictions and onerous testing regimes, or prove to be a false alarm.

After two terrible years, the industry can ill afford for 2022 to be a replay of 2021, with recovery hopes killed off by new virus variants.

🤞