Full year Heathrow passenger figures for 2022

Overall passenger volumes for 2022 down 24% on 2019

Back in October last year, I wrote about how the UK’s biggest airport was faring as the airline industry finally emerged from the pandemic in my article “Heathrow: taking stock after the pandemic”.

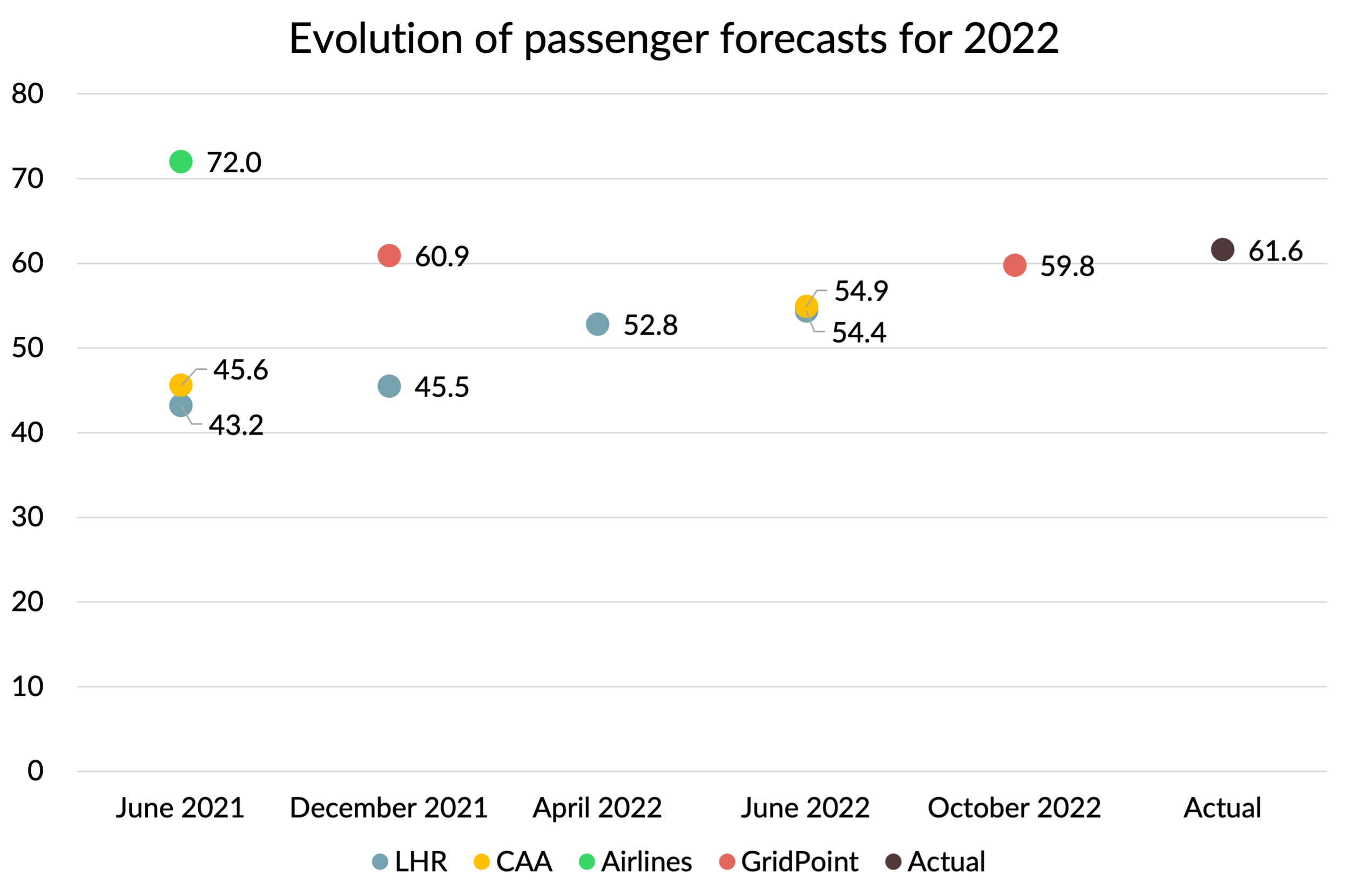

One of the topics I explored was the huge mismatch between the airport’s own forecasts for 2022 passenger traffic and those coming from airlines and other commentators, including me. The airport spent the year lobbying its regulator, the CAA, to allow it to put up landing fees per passenger by eye-watering amounts. It justified the need to do that with “low-balled” forecasts for passenger numbers. The airlines had the opposite incentive and put forward much more optimistic forecasts. When the CAA set the fees for 2022 back in June 2021, it adopted a figure between the two, but very close to Heathrow’s figures.

I’ve set out the various “forecasts” for 2022 passenger numbers in the chart below. It’s the same chart as I included in my earlier article, but I’ve now been able to add the actual outturn of 61.6m passengers. No surprises that this was way above Heathrow’s initial 42.2m forecast. It was of course also below the airline’s “high-balled” forecast of 72.0m passengers. If the CAA had “split the difference” between the airline and airport forecast they would have done much better than they did, although they would still have been too low. For the record, getting to the actual outturn would have required giving a weight of 64% to the airline view and 36% to the airport view. Perhaps the CAA might want to file away that “rule of thumb” for future reference.

My own forecast of 60.9m, made in December 2021 proved to be just 1% too pessimistic. After the operational problems of the summer, with Heathrow capping passenger numbers, I revised my forecast down a bit to 59.8m, describing it as a “reasonably conservative forecast” at the time. In reality, passenger numbers finished the year more strongly than this forecast assumed.

Performance by region

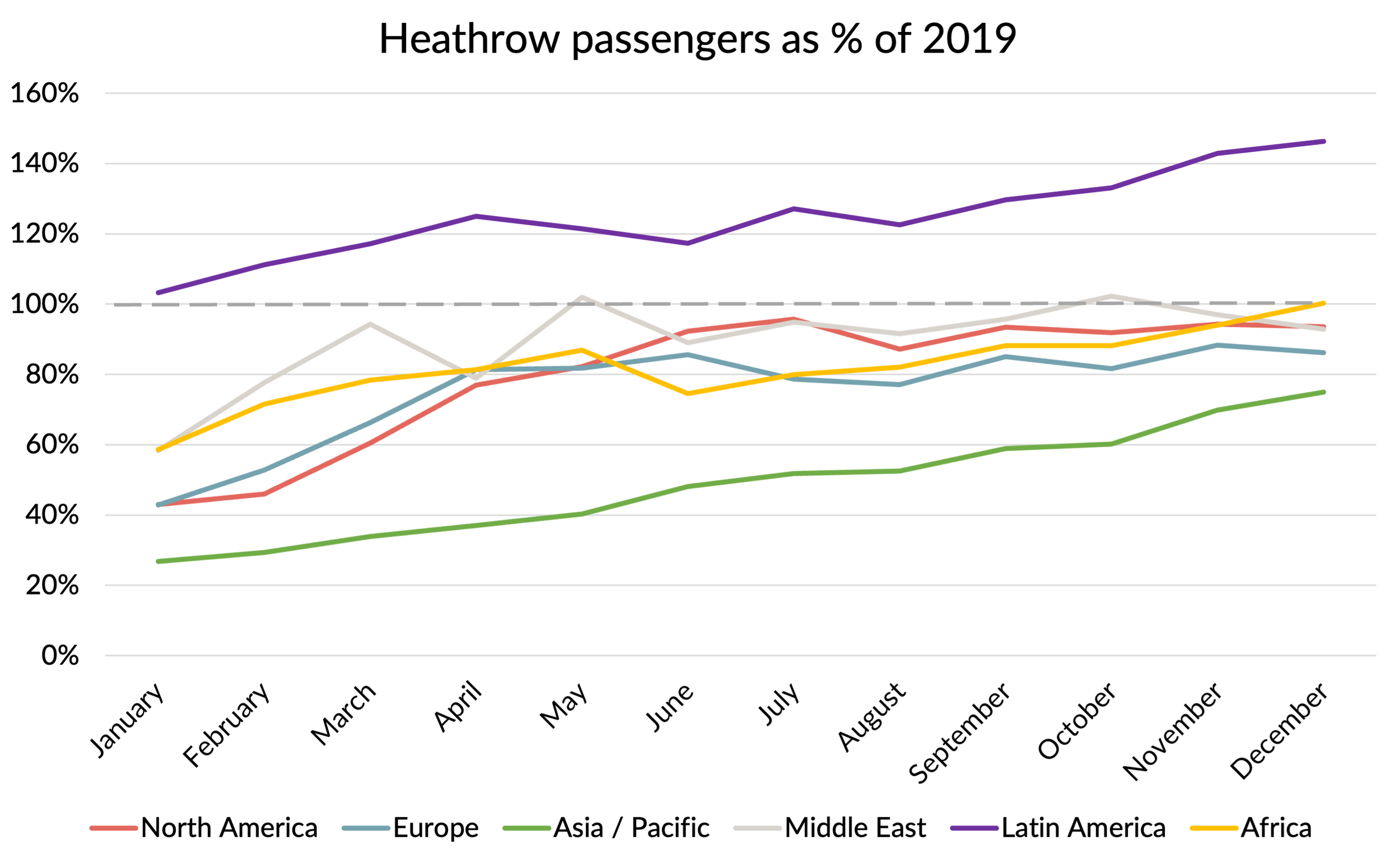

The full year total equated to 76.2% of 2019 levels, although the last two months of the year were much stronger at 89.2% for November and 88.8% for December.

It is also interesting to see how the recovery played out by region (see next chart).

The best performing region was “Latin America”, which in Heathrow’s statistics includes the Caribbean. That was 43% above 2019 levels in December, benefiting from Virgin Atlantic abandoning Gatwick during the pandemic and consolidating its flights at Heathrow. The second strongest performer in the month was Africa, which hit 100% of 2019 levels, probably thanks to good traffic to South Africa. Heathrow’s biggest long-haul market, North America, also continued to strengthen, hitting 94% in both November and December. The Middle East ended the year at a similar level.

European traffic continues to improve too, but still lags a bit behind, finishing the year at 86%. Asia/Pacific routes have been the slowest to recover, due to ongoing COVID restrictions there, compounded by European airlines’ inability to overfly Russia. Despite those issues, the region has continued to recover, hitting its best performance of the year in December at 75% of 2019 levels.

Source: Heathrow, GridPoint analysis

Prospects for 2023

What can we say about the outlook for passenger volumes in 2023?

I haven’t looked at the issue in detail, but published schedules for 2023 suggests that seat capacity at Heathrow will be virtually back to 2019 levels at 98%. There will probably be a few cancellations as we get closer to the day of operation, but with 2022 ending with passenger numbers at 88% of 2019, the “credible range” for passenger numbers would I think be 90-95% for the year as a whole, or 73-77 million passengers.

My bet would be on the upper end of that range, so 75 million or better.