Heathrow’s Q3 results. Is it crying wolf to the CAA?

A dive into Heathrow’s latest financial results

Yesterday, Heathrow reported results for the nine months ending September. It clocked up £1.5 billion pre tax losses for the year to date.

It also used the occasion to reiterate its case that it should be allowed by the regulator (the CAA) to pass on its losses to airlines and customers through an amendment to the maximum prices it is allowed to charge in future. It has been arguing that it needs urgent help from the CAA, warning of dire consequences for future investment if its shareholders are not granted a COVID “get out jail free” card.

What did the Q3 results tell us about whether the airport is in genuine financial distress, or is it just crying wolf?

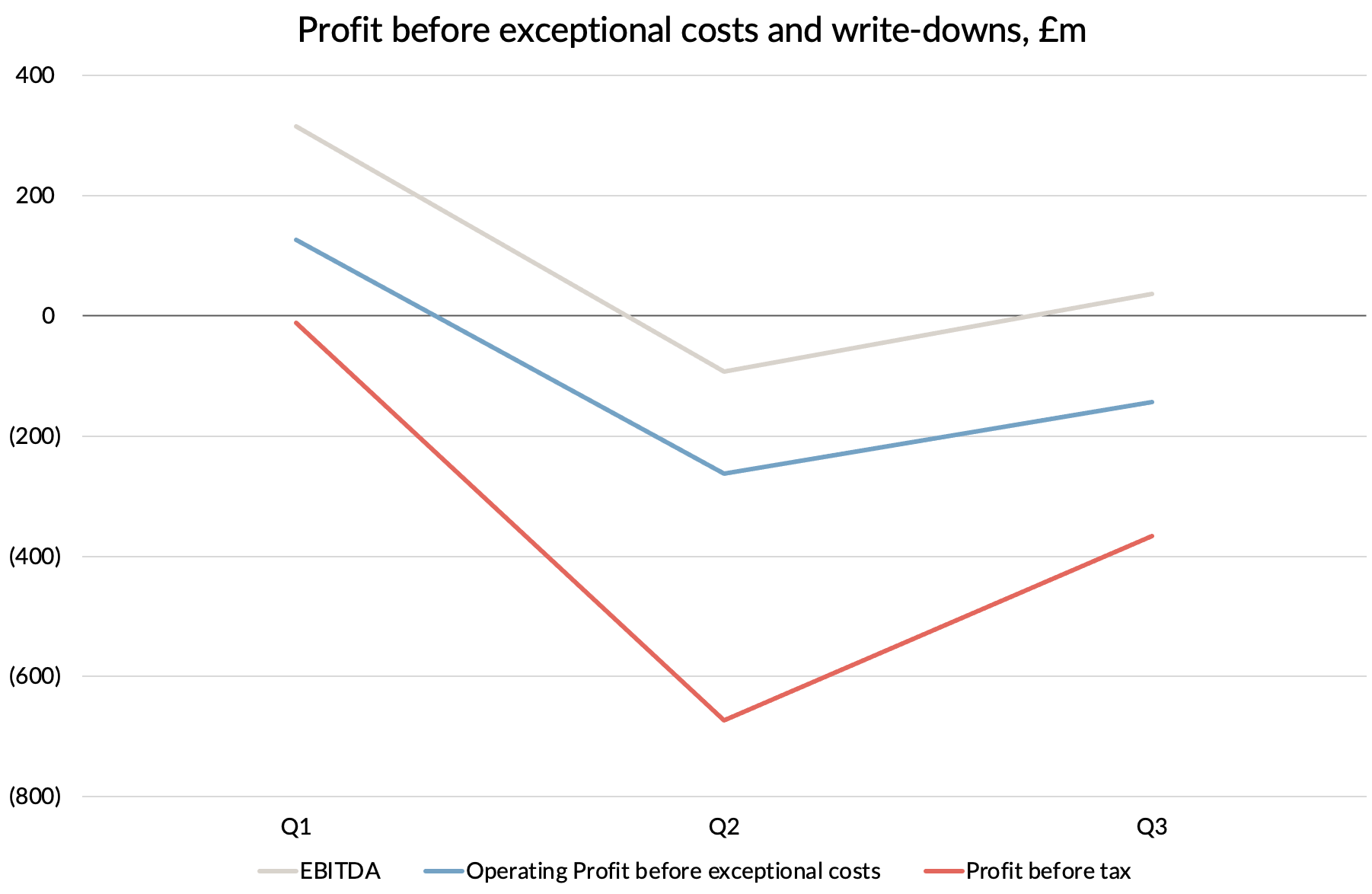

Q3 results

Isolating the results for the third quarter by itself, we find the airport made a pre-tax loss of £458m, quite a bit better than the second quarter when it lost £781m. Excluding severance costs and asset write-downs, the pre-tax loss was £366m, almost halving Q2's £673m loss.

That loss may sound big, but Heathrow’s customer airlines are making losses many times greater, with IAG having just reported pre-tax losses of £1.3 billion in Q3, 3.5 times greater.

Whilst the airport was still loss-making at the pre-tax level in Q3, earnings before interest, tax, depreciation and amortisation (EBITDA), crept back into positive territory for the first time since the pandemic hit.

The reduction in losses was driven by some recovery in revenue, with passenger numbers down "only" 84% compared to last year, much better than Q2's 96% drop. Costs overall were virtually unchanged compared to Q2.

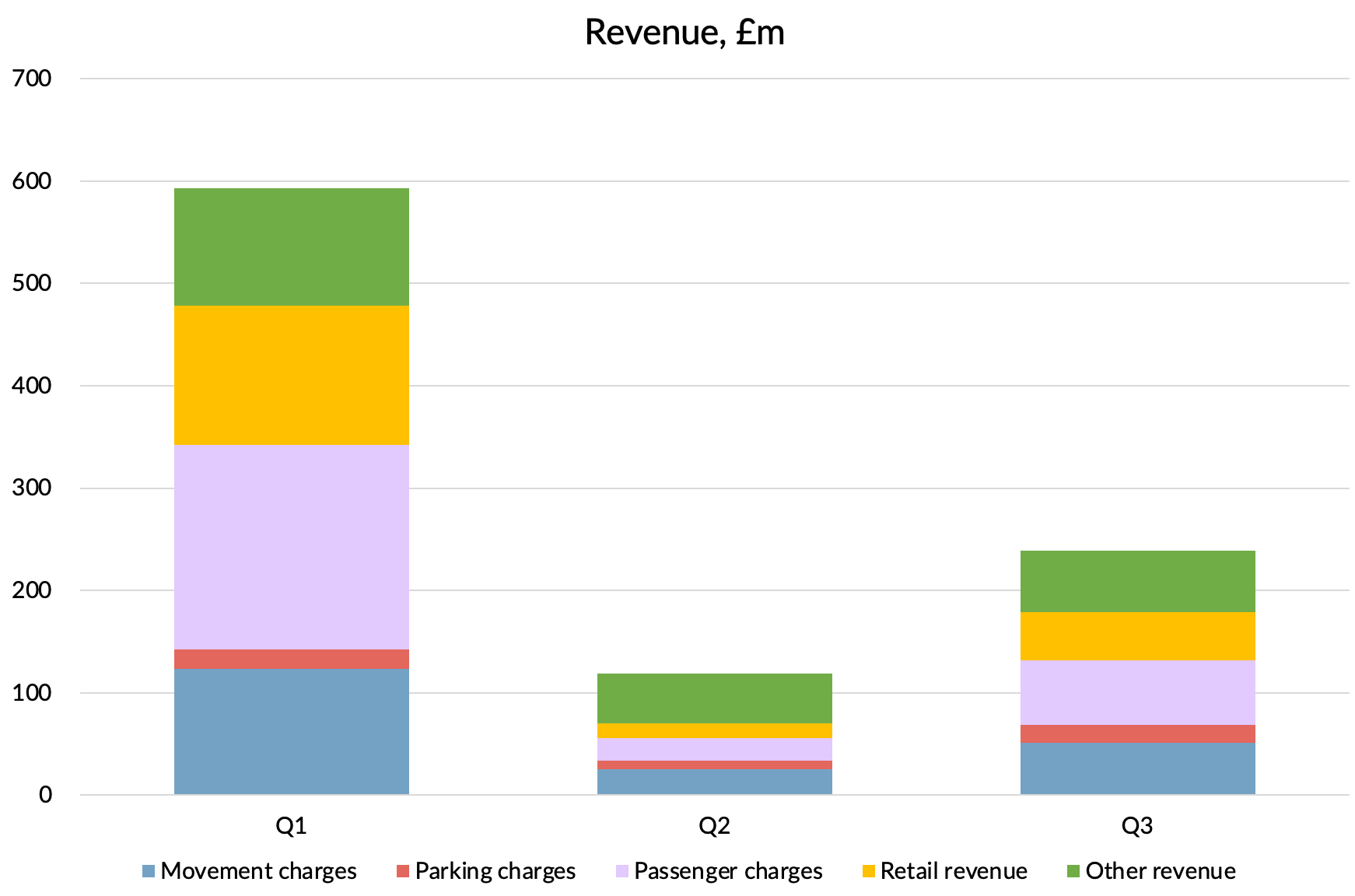

Where did the revenue improvement come from?

Aeronautical revenue

Aeronautical revenue is made up of the fees that Heathrow charges to airlines for using the airport. Some are charged per passenger, some are levied per ATM, ("Air Traffic Movement" - a landing or a take-off) and some are charged for parking aircraft. The maximum fees are regulated and Heathrow's discounts are negligible, so you would expect these revenue streams to follow the volume drivers quite closely.

Curiously, that didn't seem to be fully the case. The largest revenue category, passenger charges, fell by 82%, but that still represents an 11% increase in the per passenger charge.

The gap was even bigger when it comes to aircraft movement charges, which fell by 64% compared to passenger movements down 71%. I guess that was driven by the growth in cargo only flights which still attract fees but aren't included in Heathrow's "Passenger ATM" statistics. Cargo tonnage was down only 32% on last year, with cargo-only flights stepping into the gap left by the loss of cargo capacity on wide-body passenger flights.

The last and smallest category is aircraft parking charges, which were flat compared to last year. In Q2, they were down 50% as the airport presumably waived some charges or airline parked their aircraft elsewhere.

Overall aeronautical fees per passenger were up 60%. That's an unwelcome unit cost increase for airlines. Granted, that was mostly driven by poor load factors, which fell from 92.5% last year to only 50% this year, shocking for what would normally be peak season. Overall seat capacity through the airport was down 70% compared to last year.

Retail revenue

Retail revenues from shops, restaurants and car parking fees fell by 76%, again much less than passenger numbers. Overall retail revenue per passenger was up 47%. Presumably this was driven by fixed elements in the deals with the retailers, as it is hard to believe that actual retail spend per passenger has gone up during the pandemic.

So, a unit cost increase for retailers too then. It is clear that Heathrow has no intention of discounting its fees to attract business or help out struggling airlines and retailers.

I can hear your gasps of shock and surprise.

Volume risk

During regulatory pricing reviews, Heathrow likes to claim to the CAA that it take full "volume risk" on passenger numbers. It says that to support its arguments for being allowed to earn a higher return on capital. Based on total revenue behaviour in Q3 compared to last year, the reality seems to be that total revenues are actually only 85% variable with passengers. Still mostly variable, but an interesting data point for the CAA nonetheless.

Heathrow has now decided to “refine” its argument about volume risk. Apparently, it is only supposed to take "normal" volume risk, i.e. a few percentage points up and down. It wants the CAA to allow it to recover the “exceptional” lost revenues it is now seeing through higher prices for airlines and passengers out into the future.

It warned that if the CAA does not acquiesce to its demands, all sorts of dire consequences will ensue:

It will need to make further permanent headcount reductions, which would have a significant impact on service and costs as the airport returns to normal operations

Investment will continue to be drastically curtailed

The required cost of capital will increase considerably

The viability of expansion will be at stake

Heathrow will not be able to give airlines the support they need to help re-establish traffic

Some of these are rather laughable. Given the long lasting impact of the pandemic on traffic levels, investment needs to be drastically curtailed in any event. The runway 3 expansion plan was already in its coffin even before the pandemic nailed the lid shut. In relation to point 5, I’m sure the airlines will be only too happy to give extra money to the airport so that it can use it to help them re-establish traffic.

WTF?

Heathrow’s proposal to recover its pandemic losses

The mechanism the airport’s owners have proposed to recover their losses is to add £1.7 billion to the "RAB" (Regulatory Asset Base). That is the notional value of Heathrow’s assets, used as a key input for determining the prices it can charge, along with the previously mentioned allowed rate of return. The current RAB value is £16.5 billion, so that would be a 10% increase, or about 70% of what it cost to rebuild Terminal 2.

That would further widen the gap between the RAB and the book value of the assets in the accounts, which is more like £12 billion. Heathrow claims that it is only seeking to recover 77% of its expected lost revenues, as it is graciously volunteering to bear the first £0.5 billion of lost revenue. But the way the regulatory process works is that anything added to the RAB is not just recovered from airlines and passengers, the company is allowed to make a profit on it too. Heathrow is asking the CAA to treat the lost revenues as an "investment" by the company, on which it should be allowed to earn a return.

So far the CAA has rejected Heathrow’s proposal, but in the weakest possible way, saying:

"HAL has not, at this stage, provided sufficient information to warrant short term regulatory intervention"

But it left the door open with:

"if, in response to this consultation, HAL provides further evidence of short term difficulties, including in relation to its incentives to invest or financeability, we will assess this evidence carefully".

Airlines will remain firmly on guard about the CAA caving in to pressure from Heathrow, as the airport has clearly not given up. In it’s Q3 results statement, Heathrow said:

"We intend to respond robustly to the CAA with the required evidence."

So how much financial difficulty are Heathrow in and what "self help" steps has it taken to offset the loss of revenue by cutting costs? Let’s see what we can glean from the Q3 results.

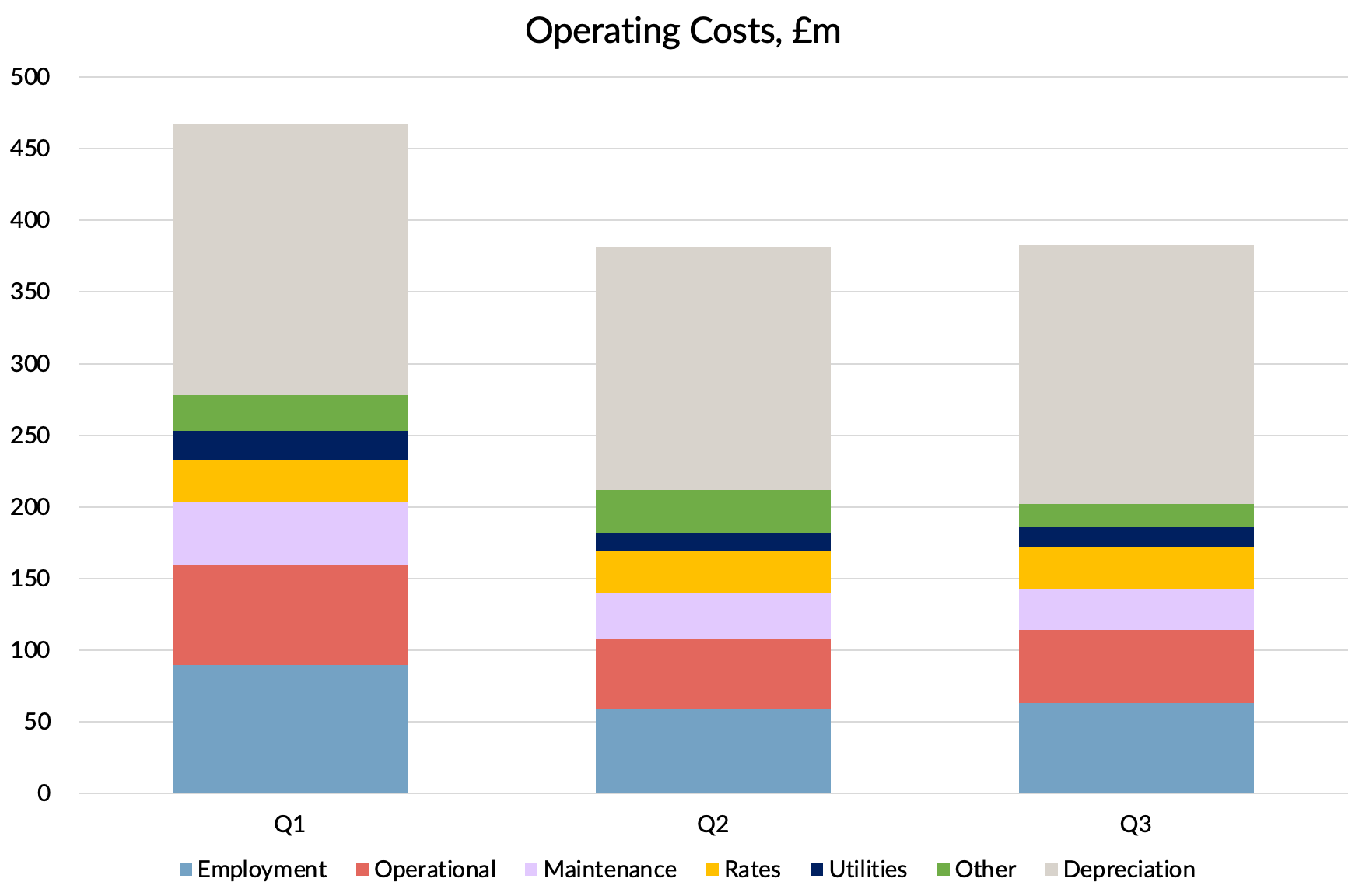

Operating costs

As I mentioned earlier, operating costs were essentially flat compared to Q2 and down only 20% compared to last year.

Employee costs, Heathrow's biggest cost after depreciation, were down 33%, helped in part by money from the UK government under the COVID-19 furlough scheme. Without that costs would have been down by 22%.

Heathrow's biggest customer, IAG, won't be too impressed by that. Faced with a similar hit to revenues, it managed to bring down its employee costs by 50% in Q2 and I expect them to do something similar in Q3.

Cash levels

Revenues may be heavily down, but at £239m in the quarter they were more than enough to cover £202m of cash operating expenses, meaning EBITDA was positive as we have already seen.

Heathrow has slashed capital expenditure by 68%, so it only spent £73m on that. That was actually covered by the £72m tax rebate it got in the quarter. Those rebates should continue whilst the airport continues to lose money.

There were £60m of cash costs related to severance in the quarter, but those are one-off and some negative working capital effects that shouldn’t recur either. So I think that Heathrow's only real challenge is how to cover the cost of servicing its debt whilst revenue remains at current levels.

Cash interest costs added up to £160m in Q3, plus £10m of lease payments. Interest costs fell by 22% versus last year, with Heathrow commenting that the average interest cost on its debt fell from 3.41% last year to 2.55%, benefiting from the continuing decline in interest rates. The only reason that these costs are as high as they are is because Heathrow’s owners have chosen to load the company up with debt in order to boost their equity returns. They run the company at significantly higher gearing levels than are assumed by the CAA when assessing the cost of capital. OK, that is their choice, but the flip side of that gamble is that they will need to inject equity if profitability falls.

In any case, we seem to be some way away from that. The company had £2 billion of cash and term deposits at the end of September and so has plenty of cash to continue to meet its interest costs for quite some time, even without a recovery in revenue. There will be debt repayments to make as well, but Heathrow seems to be having no problem raising new debt at the moment, almost certainly replacing old debt with new at lower interest rates. It raised another £1.4 billion of new debt in October and also secured another £750m facility.

In conclusion

From what I can see, Heathrow isn’t in financial difficulty. It’s shareholders might be unhappy and worried about the need to inject equity capital at some point. But I would wholeheartedly agree with the CAA's statement that the evidence "falls short of that required robustly to justify its claims that “urgent support/action is necessary” and that any such support should be in the form and of the scale in HAL’s request."

The airlines and their customers will hope that the CAA continues to take a robust line in rejecting Heathrow's arguments.

Only a company with the arrogance of Heathrow could be vocally lobbying to be allowed to shield its shareholders from the consequences of the pandemic and their own decisions to load up the airport with debt. Especially when that would offload the airport’s pandemic losses on its customers, all of whom are suffering vastly more than the airport is at the moment.